Fortinet was founded in 2000 and is headquartered in Sunnyvale, California. The company provides broad, integrated, and automated cybersecurity solutions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Introduction

Fortinet provides security subscriptions, technical support, and professional, and training services. It sells its security solutions to channel partners and directly to various customers in telecommunications, technology, government, financial services, education, retail, manufacturing, and healthcare industries.

- FortiGate hardware and software licenses that provide various security and networking functions, including firewall, intrusion prevention, anti-malware, virtual private network, application control, web filtering, anti-spam, and wide area network acceleration.

- FortiSwitch product family, offers secure switching solutions for connecting customers to their end devices.

- The FortiAP product family, provides secure wireless networking solutions.

- FortiExtender, a hardware appliance.

- FortiAnalyzer product family, which offers centralized network logging, analyzing, and reporting solutions.

- FortiManager provides a central and scalable management solution for its FortiGate products.

- FortiWeb provides web application firewall solutions.

- FortiMail secures email gateway solutions.

- FortiSandbox technology delivers proactive detection and mitigation services.

- FortiClient provides endpoint protection with pattern-based anti-malware, behavior-based exploit protection, web filtering, and an application firewall.

- FortiToken and FortiAuthenticator product families for multifactor authentication to safeguard systems, assets, and data.

- FortiEDR/XDR, is an endpoint protection solution that provides both comprehensive machine-learning anti-malware execution and real-time post-infection protection.

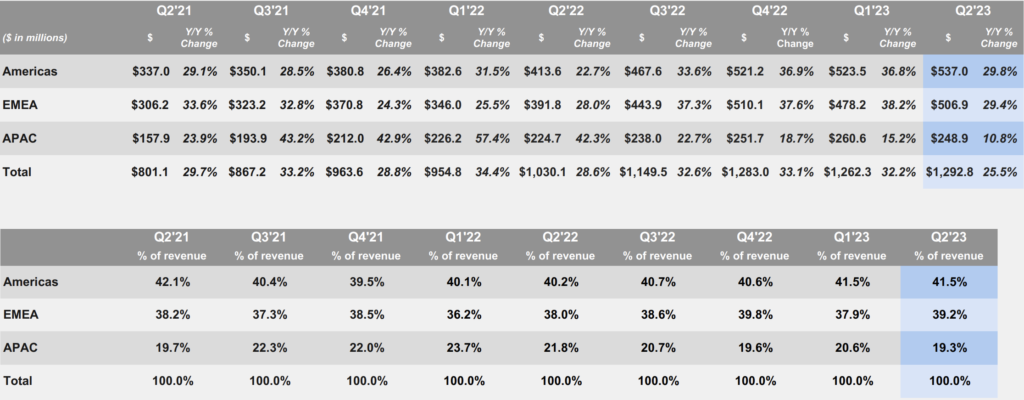

Revenue by Geography (Q2 2023)

According to their last earnings call, we see how Fortinet has been gradually increasing revenue in all territories since 2021, and Americas is the highest revenue provider compared to EMEA and APAC.

Market Research and Forecast

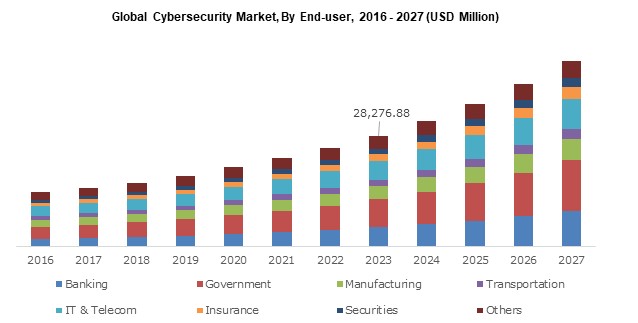

The global Cybersecurity market has been growing since 2018, especially in North America, Europe, and Asia Pacific, where the North American market is the sector’s most important demand and where Fortinet has more get the vast majority of its revenue. According to Polaris, North America will still be the leading region until 2030, followed by Europe and Asia Pacific.

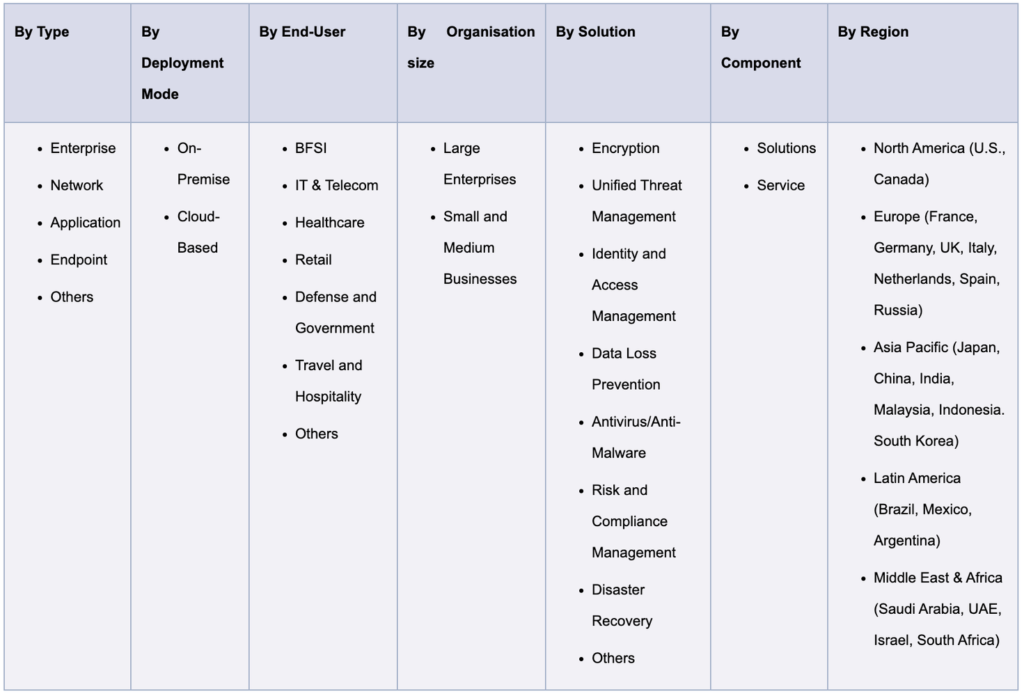

The market is segmented based on type, deployment model, end-user, organization size, solution, component, and region.

Security Services dominates the market with a projected market volume of US$87.97bn in 2023.

The three main cybersecurity consumer groups are the banking and IT and telecom industries followed by Governments, where logically this last group leads the demand, according to GM Insights.

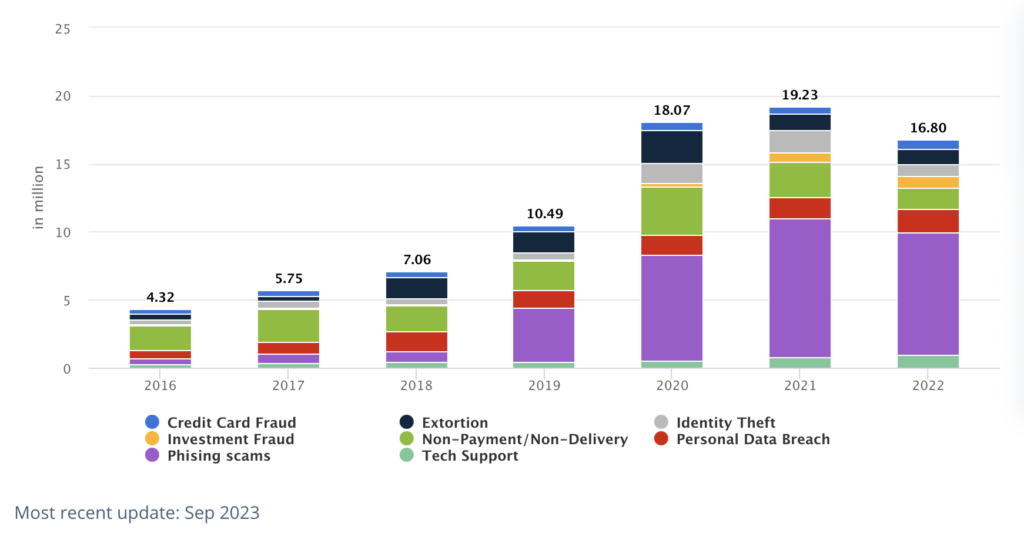

Another factor to take into consideration that explains the demand for cybersecurity services is the continuously growing trend of cyberattacks, where phishing scams took the lead in 2019.

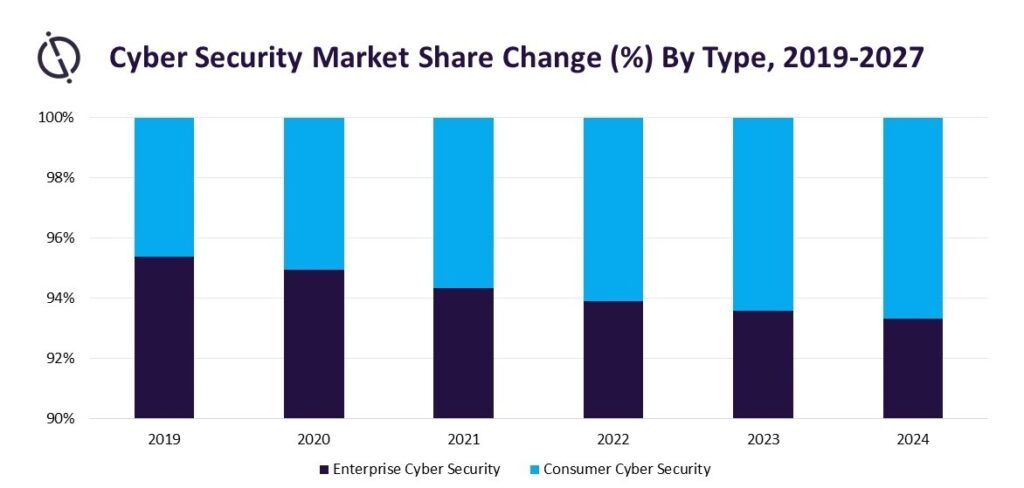

That being said, and according to Globaldata, we can see a change in the current paradigm where Consumer Cybersecurity is expected to grow and take more market share than the Enterprise demand.

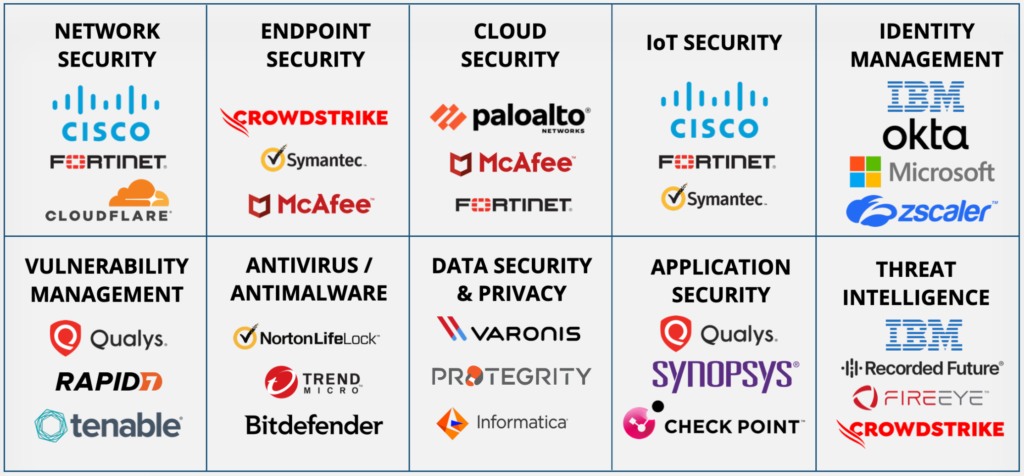

Finally, in the image below you will find how the cybersecurity market is composed (and how big it is). According to Fortinet, the main company business pillars are Network Security, Cybersecurity, Cloud Security, and OT Security.

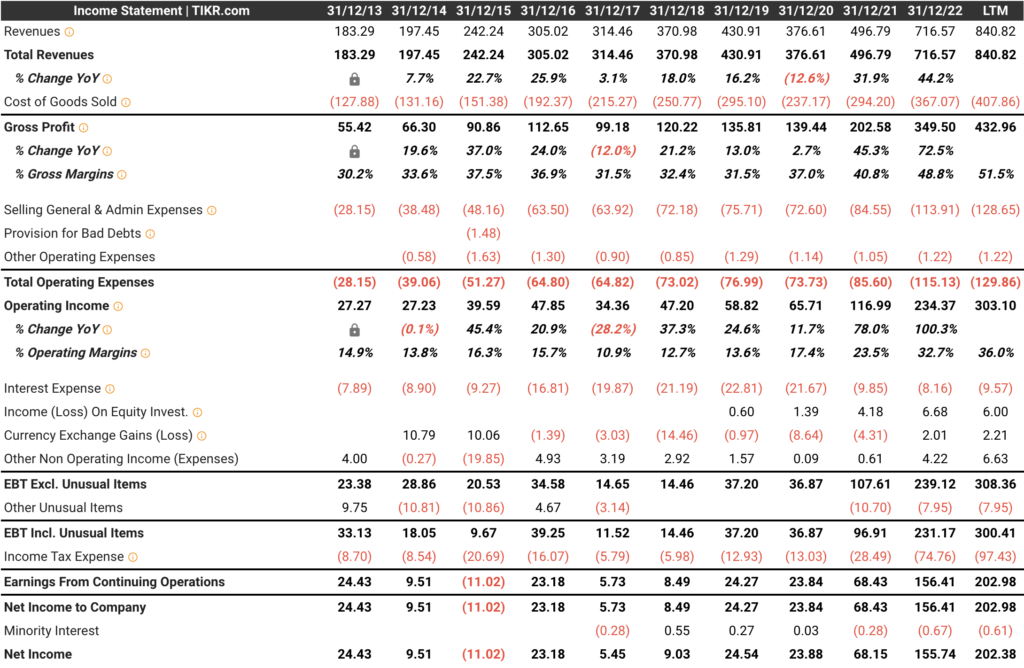

Fortinet Income Statement

Fortinet has demonstrated strong results over the last 10 years by keeping high and consistently growing Revenue double-figure and greater than 29% since Q2’21 according to their last Q223 Earnings Call, but also, sustainable Gross Margins which have been greater than 70% since 2013, which is a really positive indicator of a healthy business.

In 2014 and 2015, with the operating expenses raised, the Operating Income decreased by (21.9%) and (57.1%).

The Sales and Marketing and General and Administrative were the items that received the greatest investment, taking into account its Annual report (10K):

“In 2015, we continued to invest in sales and marketing to capture market share, particularly in the enterprise market where enterprise customers tend to have a higher lifetime value, and to accelerate our growth. We intend to continue investing in sales and marketing in order to capture additional market share in the enterprise market”.

The global sales and marketing employee footprint increased from 41% in Q1 to 44% in Q4, as well as their investment, according to the company’s quarterly reports:

“In 2015, operating expenses increased by $227.6 million, or 47%, as compared to 2014. The increase was primarily driven by our accelerated pace of hiring and continued investments to expand our sales coverage, grow our marketing capabilities, develop new products and scale our customer support. We also continue to invest in research and development to strengthen our technology leadership position. We believe that continued product innovation has strengthened our technology and resulted in market share gains. In addition, we incurred costs from the integration of Meru and the implementation of restructuring activities and expenses related to business design and reengineering in preparation of an ERP system implementation. Headcount increased by 41% to 4,018 employees and contractors as of December 31, 2015, up from 2,854 as of December 31, 2014.“

Source: Fortinet 10-Q

In regard to the headcount increase, in July 2015, Eric Mann and Mike Bossert joined the company’s leadership team, as sales vice presidents focused on continued expansion and growth of the enterprise and mid-enterprise market segments, and in September of the same year, Fortinet announced that Holly Rollo joined as Chief Marketing Officer.

Additionally, the company expanded its patent portfolio to more than 200 patents.

Back in 2018, we can see positive Income Tax Expenses as a result of effective tax rate benefits.

Our provision for income taxes for 2018 reflects an effective tax rate benefit of (32)%, compared to an effective tax rate provision of 75% for 2017. The benefit from income taxes for 2018 was comprised primarily of impacts related to the 2017 Tax Act including a benefit of $164.0 million from the realignment of our tax structure and operations that resulted in a book-to-tax basis difference from previously taxed off-shore deferred revenue. These benefits were partially offset by a $32.6 million increase in the transition tax for finalization of the provisional estimates under SAB 118, a $20.5 million tax expense for the impact of the GILTI and a $29.6 million of tax expense related to U.S. federal and state taxes, other foreign income taxes, foreign withholding taxes and a decrease in tax reserves. Effective January 1, 2018, the 2017 Tax Act reduced the federal corporate income tax rate from 35% to 21% and created a territorial tax system with a one-time mandatory tax on foreign earnings of U.S. subsidiaries not previously subject to U.S. income tax. Under GAAP, changes in tax rates and tax law are accounted for in the period of enactment and deferred tax assets and liabilities are measured at the enacted tax rate. In December 2017, the SEC staff issued SAB 118, which allowed us to record provisional amounts during a measurement period not to extend beyond one year of the enactment date. As a result, we previously provided a provisional estimate of the effect of the 2017 Tax Act in our financial statements. In the fourth quarter of 2018, we completed our analysis to determine the effect of the 2017 Tax Act within the measurement period under the SEC guidance, and reflected an increase of an additional $32.6 million related to the transition tax in the 2018 income tax expense. We expect further guidance may be forthcoming from the FASB and the SEC, as well as regulations, interpretations and rulings from federal and state tax agencies, which could result in additional impacts. In 2017, the effective tax rate was 75%, primarily resulting from the deferred tax assets remeasurement and a one-time transition tax due to the 2017 Tax Act. Excluding the tax impacts from the 2017 Tax Act, our 2017 effective tax rate would have been 24%.

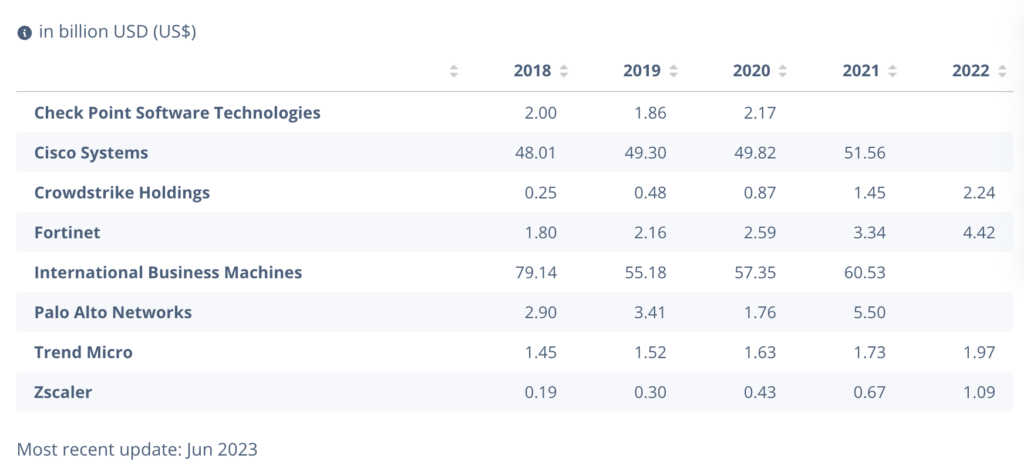

According to a report from Statista released in June 2023, Fortinet has built on an upward revenue trend from 2018 to 2022 that has allowed it to expand and distance itself from some of its competitors, that being said, the company is still far from big players like Cisco or International Business Machines but its constant and bullish trend is a good sign of thriving business, especially if we take into account the external factors on 2020 and how negatively impacted in some business, due to Fortinet biggest factories are in Taiwan and China.

On the other hand, According to IDC (the world’s leading provider of market intelligence, consulting services, and events for the Information Technology, Telecommunications, and Consumer Technology markets), Fortinet Firewall division solution surprises in Revenue market share in 2022 to Palo Alto Network, Cisco and Check Point and kept a comfortable distance in 1QC 2023.

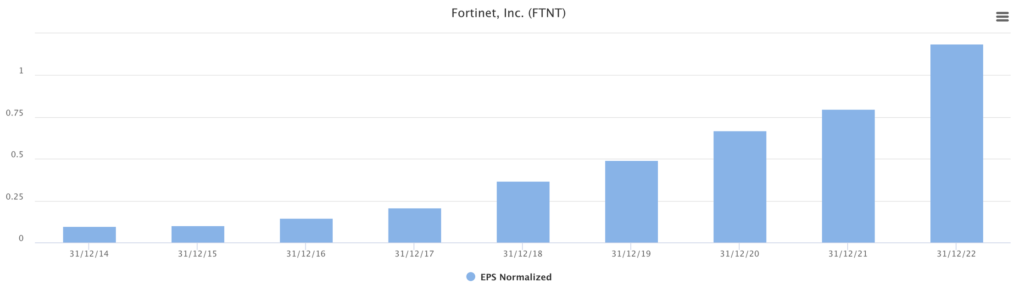

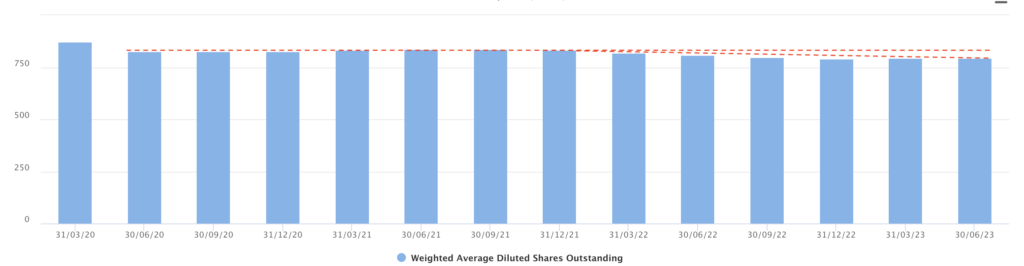

Fortinet has reported sustainable EPS growth (37% average CAGR from 2015 to 2022).

If we take a look at their Operating Expenses in 2023, we should take into account that Fortinet has a total of 1,285 global patents (as of June 30, 2023) and 254 Pending Patents, which makes me better understand the continuous increase is logical together with the development of new technologies, may affect the raise. I do not consider a concerning figure for the sales and marketing item taking into account the YoY growth from the last 6 years of Revenue and the Gross Margins as we mentioned earlier.

Balance Sheet

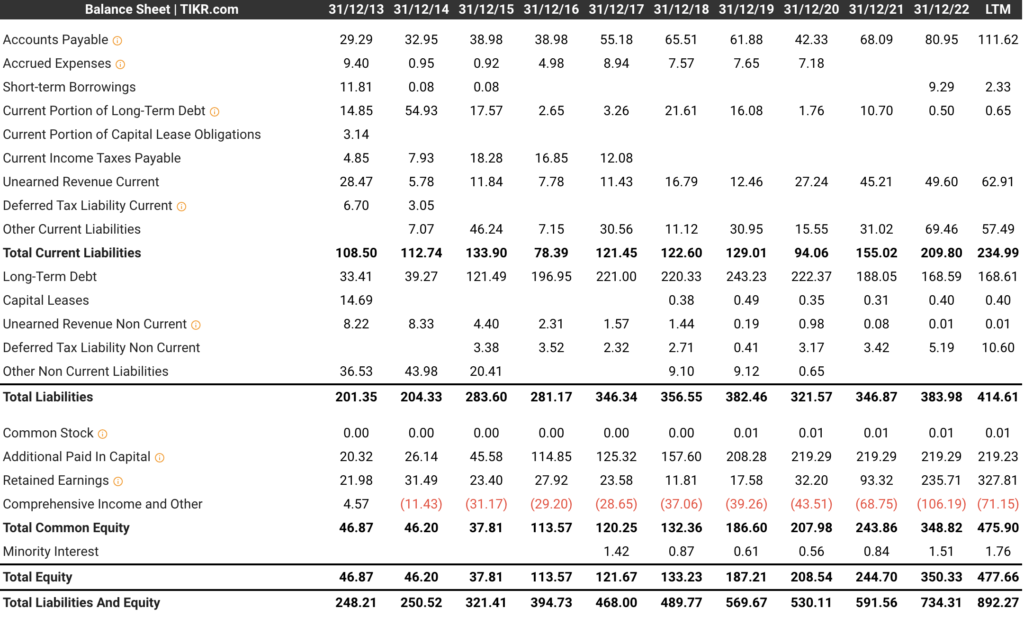

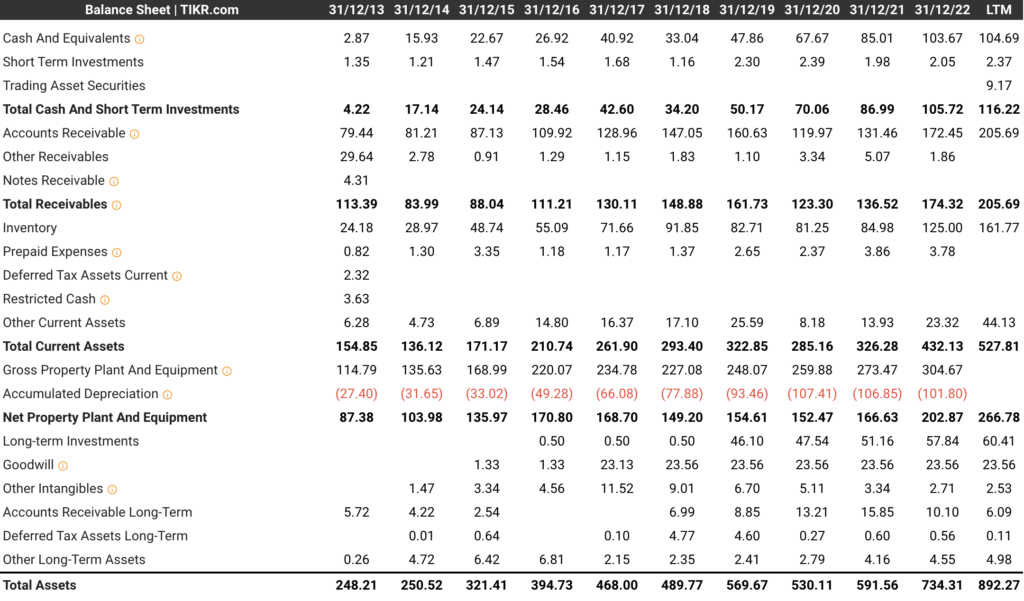

Fortinet has a positive liquidity ratio, if we take a look at its current assets vs. current liabilities, over the last 10 years the company has been above 1.2, which I consider a good ratio, and it tells us its capacity to generate liquidity in a short-term period. On the other hand, their Inventory and Net Income growing trend demonstrates a healthy and correlated selling cycle, where the volumes are still reasonable.

Long-term debt increase in 2021 comes from a Senior Notes offering where the company priced a $1 billion debt offering ($500 million in 1.000% notes due 2026 and $500 million in 2.200% notes due 2031). Additionally, the company reduced the amount of shares starting in March.

In July 2020, our board of directors approved a $500.0 million increase in the authorized stock repurchase amount under the Repurchase Program and extended the term of the Repurchase Program to February 28, 2022, bringing the aggregate amount authorized to be repurchased to $3.0 billion.

Source: Fortinet Inc 10-Q

Our principal commitments consist of obligations under our Notes, inventory purchase and other contractual commitments. As of December 31,2021, the long-term debt, net of unamortized discount and debt issuance costs, was $988.4 million. In addition, we enter into non-cancellable agreements with contract manufacturers to procure inventory based on our requirements in order to reduce manufacturing lead times, plan for adequate component supply or incentivize suppliers to deliver. In 2021, we significantly increased these commitments as contract manufacturers and component suppliers significantly increased their pricing and lead times. Inventory purchase commitments as of December 31, 2021, were $1.14 billion, an increase of $881.1 million compared to $259.4 million as of December 31, 2020. We estimate payments of $1.08 billion due on or before December 31, 2022 related to these commitments. We also have open purchase orders and contractual obligations in the ordinary course of business for which we have not received goods or services. As of December 31, 2021, we had $126.7 million in other contractual commitments having a remaining term in excess of one year that are non-cancelable.

Source: 10-K Fortinet Inc 2021

As we mentioned earlier, the pandemic hit multiple businesses (and created other investment opportunities). In 2021, and because of the pandemic, this impact on the manufacture of semiconductors in South Korea and Taiwan was cited as a cause for the shortage, so my understanding is that in order to guarantee the supply, the company.

Reviewing the investments line item, I found two big ones around 2021.

The first one is Linksys Holdings, Inc. (“Linksys”), where Fortinet invested $160 million in cash for shares of the Series A Preferred Stock of privately held representing a 50.8% ownership interest in the outstanding common stock (on an as-converted basis). Linksys provides router connectivity solutions to the consumer and small business markets, that being said, its sales have declined since Fortinet started its investment.

Last but not least, between 2021 and 2022 Fortinet executed a strategic acquisition of Alaxala Networks Corporation, a privately held network hardware equipment company in Japan, for $77.7 million in cash. According to Fortinet:

We acquired the equity interests in Alaxala to broaden our offering of secure switches integrated with our Core Platform and Enhanced Platform Technology functionality and over time, to innovate and rebrand certain of Alaxala’s switches to offer a broader suite of secure switches globally.

The company has good short-term liquidity ratios, especially the Current Ratio (total current assets / total current liabilities) which has been above 1 since 2013 and explains its power to pay down the current liabilities.

Competitors’ Pros and Cons

Fortinet’s competition is spread around the world, some names are Arista Networks, Inc., Aruba Networks, LLC, Barracuda Networks, Inc., Check Point Software Technologies Ltd., Cisco Systems, Inc. (“Cisco”), CrowdStrike Holdings, Inc., F5 Networks, Inc., Huawei Technologies Co., Ltd., Juniper Networks, Inc., Palo Alto Networks, Inc., SonicWALL, Inc., Sophos Group Plc, Trend Micro Incorporated, VMware, Inc. and Zscaler, Inc. (“Zscaler”). I believe that Fortinet has a competitive advantage over its competitors, these are some examples that led me to think so:

- Some companies have been reporting negative Net income over the last seven and then years

- Big corporations are growing slowly, which is understandable due to their global presence

- Long-term debt. I try to find companies with low long-term debt levels, but some of them have not been able to decrease it (Fortinet is not exempted). That being said, the big players with enough earning power have the advantage of being able to meet their long-term debt payments

- Liquidity levels are a bit concerning across some of their competitors, they will struggle to convert assets to pay their liabilities

But, these companies can perform better in some KPIs and have advantages:

- Better margins, above 80%

- The gap between Price and EPS is bigger than Fortinet, so they can potentially be undervalued if we compare it to their capacity to generate value for the investor

- Bigger budgets to invest in sales, marketing, and IT

- Important, Brand recognition. I do not need to mention which ones are more well-known than others

- Switching costs are key in this industry, especially if we take into account the enterprise customer and the investment in training

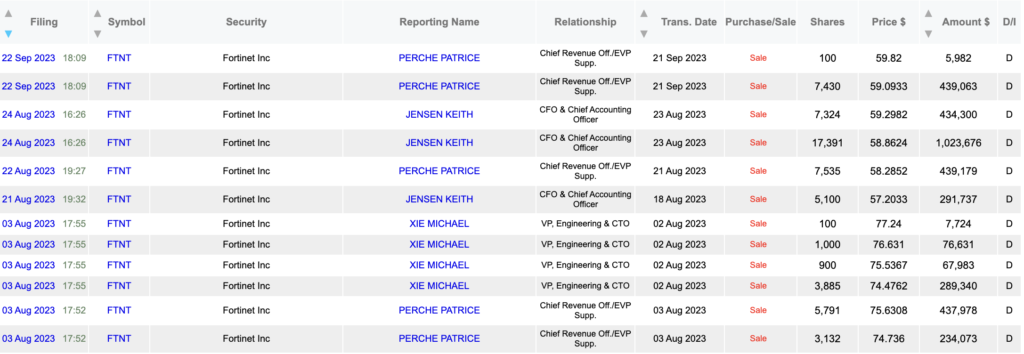

Fortinet’s Ownership

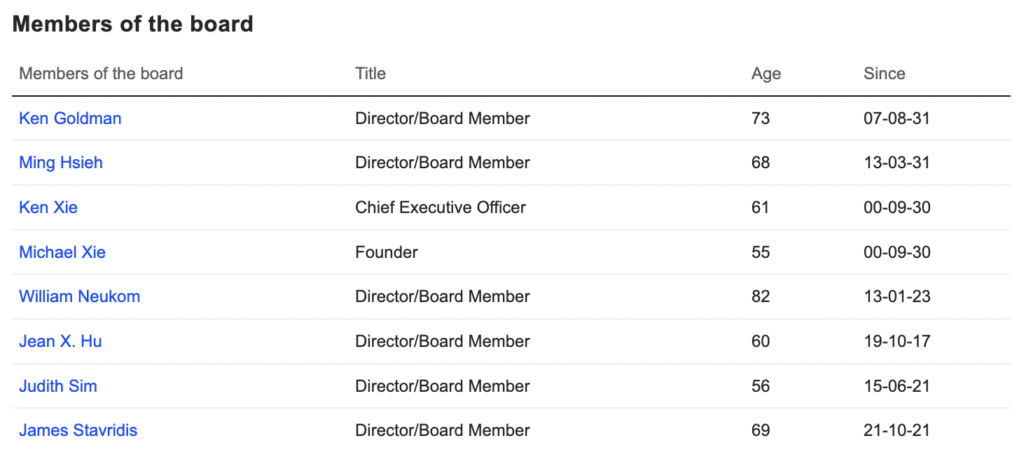

Fortinet’s CEO Ken Xie, the founder of the company, holds more than 63M shares (8% of shares outstanding held), and her brother Michael Xie, who also holds 69M (8.85% of shares outstanding held) which is a good sign not only because both have key roles in the company but also because the Xie family keeps a big share of the company, and convey a solid alignment between their and the company’s interests.

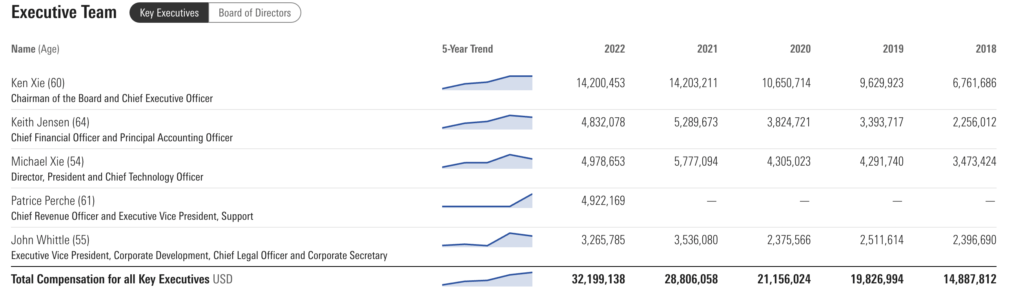

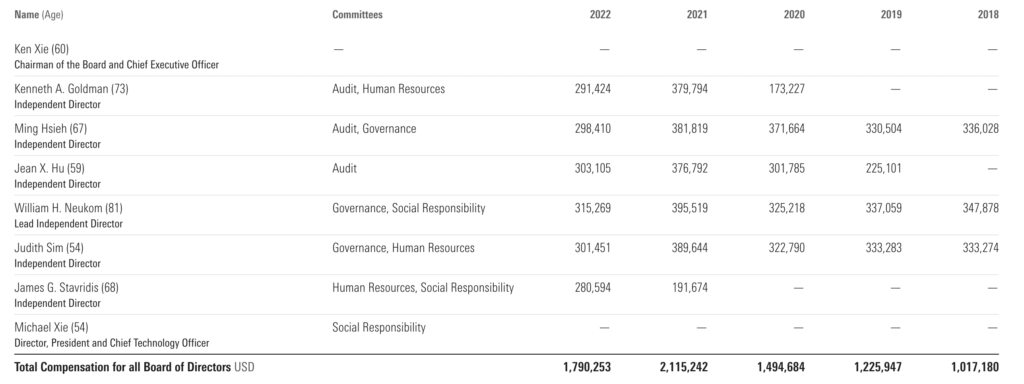

Below, I’ve included a snapshot of Fortinet’s Key Executives and Members of the Board Director, along with their yearly compensation. None of the stakeholders makes more than 10% in revenue, which is a positive sign and it makes me feel that the leadership team is not squeezing the organization funds.

Regarding the Insiders, we have not identified unexpected movements or aggressive sales from the Executive team or board of Directors.

Valuation

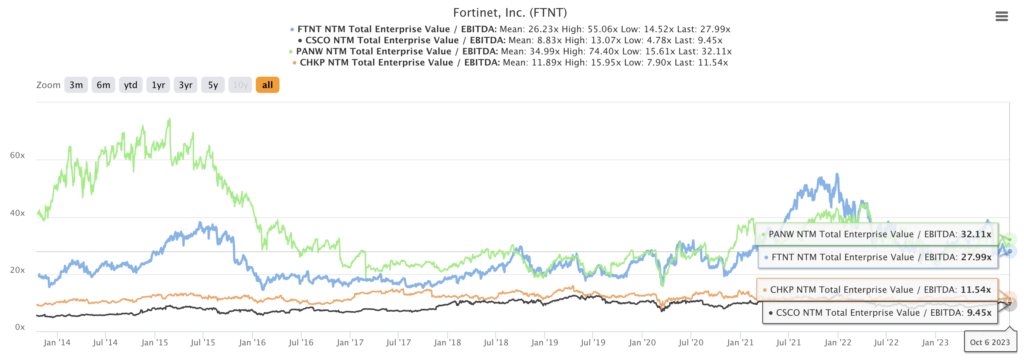

Fortinet is currently valuated at 27% EV/EBITDA. Although I believe the company does not have an attractive valuation, I would mention some key things.

- First of all, the revenue is projected to grow at double-digit and above >20%, the company is doing a great job so I consider it not exaggerated.

- The valuation is not at all-time highs, even though this is not a metric that by itself doesn’t tell me anything, the drop in we have observed it’s due to how fragmented is the market and how unclear is for Mr.Market to buy Fortinet or other cybersecurity companies.

- Reviewing its main competitors, we should break down them by like Check Point Software and Cisco, big corporations growing <10% every year with expanded worldwide, and Fortinet and Palo Alto Networks, where personally I do think Fortinet has better and robust financial health.

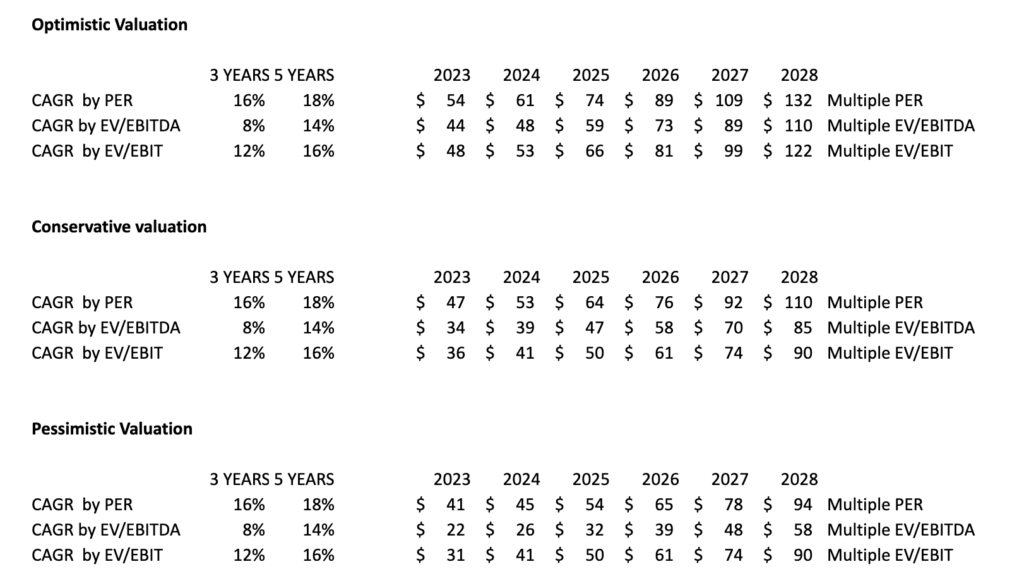

So, let’s talk about the (my) valuation.

I’ve built three scenarios by taking into account different PER, EV/EBITDA, and EV/EBIT valuations. I took into account the lowest, mid, and highest valuations not only from Fortinet but also from its competitors. To be honest, I will take into account the EV/EBITDA instead of the PER.

Final Comments

- The software industry is usually considered a monopoly business model where “Winner Takes All”, and where the cybersecurity market is very fragmented.

- Big competition means that at some point, there exists the possibility that some companies with a worse competitive advantage will increase debt as they cannot self-finance if they need funds for investments like acquiring new companies, adding more resources to increase sales, or IT to develop new technologies or finance patents.

- Fortinet’s revenue forecast CAGR (5y) is 18.8%, which is above the 15% I consider the minimum CAGR the market average and my security margin.

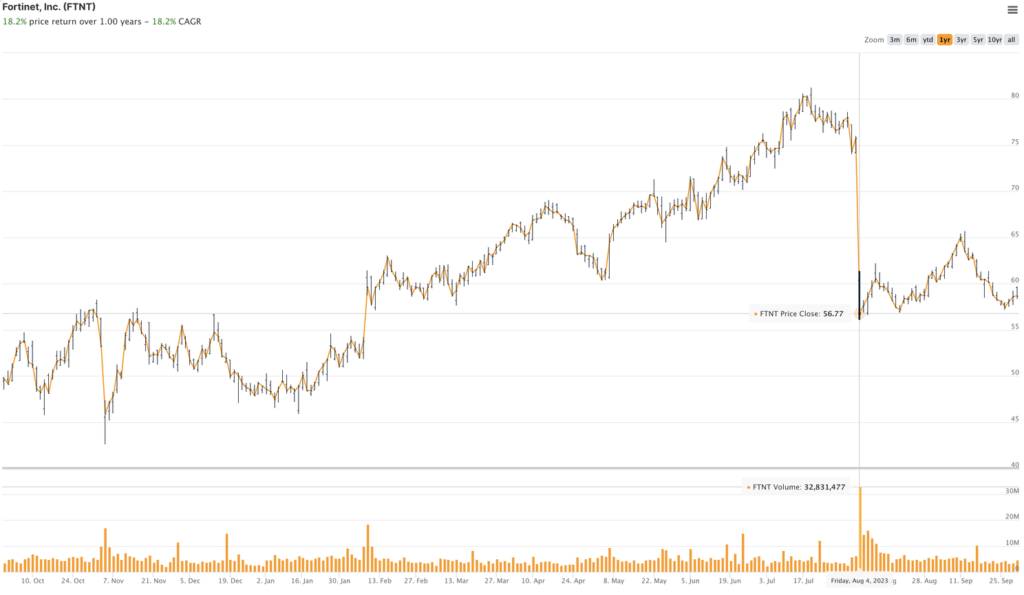

- On August 3rd, the company announced earnings and the share price decreased from $75.76 to $56.77/share (-28.65%), after the company confirmed to expect total revenue in the range of 5.35 billion to 5.45 billion for the fiscal year 2023, a lower figure from a prior view of $5.43 billion to $5.49 billion.

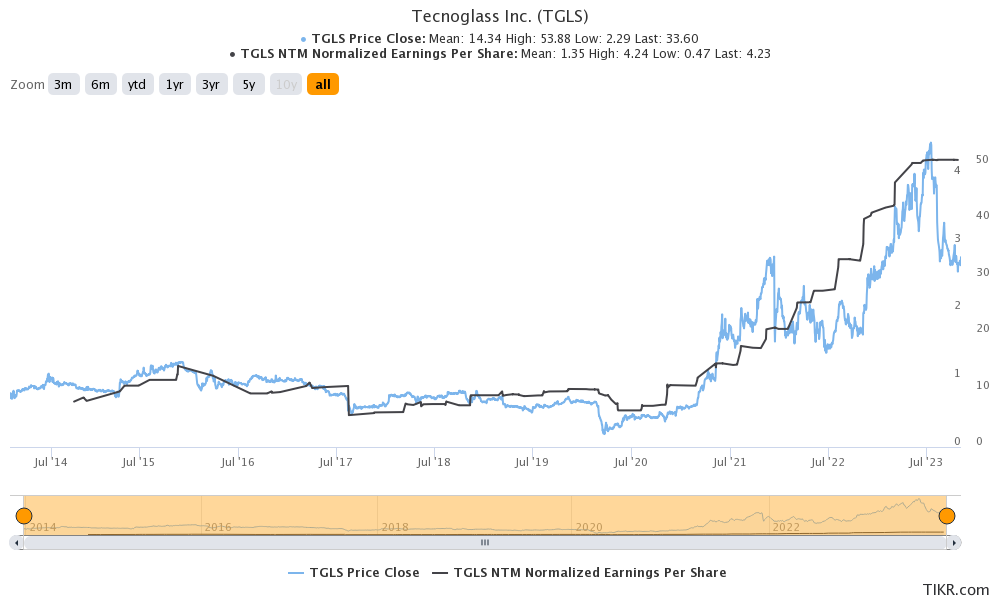

But when we take a look at the share price evolution but also the NTM Normalized Earnings per share, there is a healthy correlation between the price and the earnings growth, showcasing Fortinet’s value generator and its capacity to recover its share price in 2020 despite the global pandemic, so the drop in the stock price could be influenced by the fact that there is not a clear leader in the industry, and that can easily affect the investor’s perception vs the companies strength to capture the pole position.

That being said, the initial rate of return is not attractive (1.57$/58=2.7%), so to see an interesting rate of return figure around 12%, the price should have a correction of around 50%, and the earnings per share should increase up to 3.5$.

These books helped me to better understand the value investing: