Executive Summary

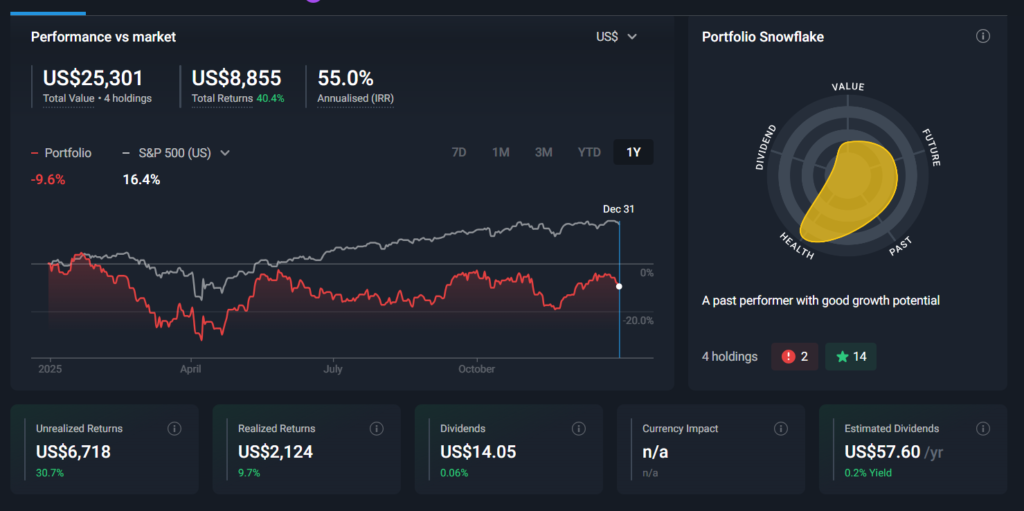

In the year 2025 the portfolio registered a total return of -9.6%, underperforming the broad SP500 benchmark which delivered +16.4% growth over the same period. This performance reflects both challenging macro conditions and idiosyncratic moves in select holdings. The portfolio accumulates a total return of +40.4%.

The portfolio comprised the following equities:

- Alphabet (Google)

- Bruker Corporation

- Fortinet

- Tecnoglass

- Tesla

- Realty Income

- Adobe (added during the year)

Key Results & Attribution

Overall Return

- 2025 Annual Return: −9.6%

- Benchmark (S&P 500): +16.4%

This gap highlights a period of reallocation and stock-specific volatility rather than broad market exposure.

Cumulative Performance since 2023

- Total Return (2024–2025): +40.4%

Major Transactions & Rationale

- Bruker Corporation

- Liquidated with a realized gain of +51.88%

- The position was sold once our internal intrinsic value estimate was breached, allowing redeployment into assets with stronger growth prospects and better risk-reward profiles.

- Sale proceeds increased portfolio liquidity and reduced exposure to cyclicality in scientific instruments.

- Alphabet (Google)

- Realized gain of +21.25%

- Traded out earlier in the cycle as price exceeded our fair value estimate, locking in gains. While the stock continued to appreciate, maintaining discipline around valuation was prioritized.

- Adobe

- New addition in 2025

- Introduced based on resilient fundamentals, solid earnings momentum, and strong competitive positioning in digital media/software.

Performance Drivers (Positive & Negative)

Positive Contributors:

- Bruker liquidation: Positive realized gains boosted absolute return before reallocations.

- Fortinet & Tecnoglass: Continued solid business performance helped mitigate some broader market weakness.

Negative Contributors:

- Tesla: High volatility and sector-wide rotation away from growth pressured returns.

- Realty Income: Sensitivity to rising rates and real estate sector softness impacted yield-oriented holdings.

Discussion & Context

- Risk & Return: The portfolio’s performance must be evaluated in the context of active stock selection and disciplined rebalancing, rather than passive benchmarking. Absolute losses reflect idiosyncratic exposure as well as strategic reallocations in the face of market uncertainty.

- Valuation Discipline: Systematically selling positions once they exceed our intrinsic value estimates has supported capital preservation and disciplined reinvestment.

- Exposure Review: Allocation shifts during 2025 reflect a bias towards companies with stronger competitive moats and growth visibility.

2026 Priorities

- Rebalance Exposure: Consider incremental diversification across sectors and factors (e.g., defensive, value, small caps) to balance growth risk.

- Monitor Macro Signals: Rate trends and valuation compression remain critical for equity performance.

- Refine Metrics: Incorporate risk-adjusted performance indicators (e.g., Sharpe Ratio) and attribution analysis to better isolate decision impact versus market movements.

Conclusion

While 2025 delivered a negative annual return, performance must be interpreted through the lens of active management and valuation discipline. The portfolio remains positioned to capture growth in selected secular trends, supported by a robust cash position and rigorous valuation frameworks.