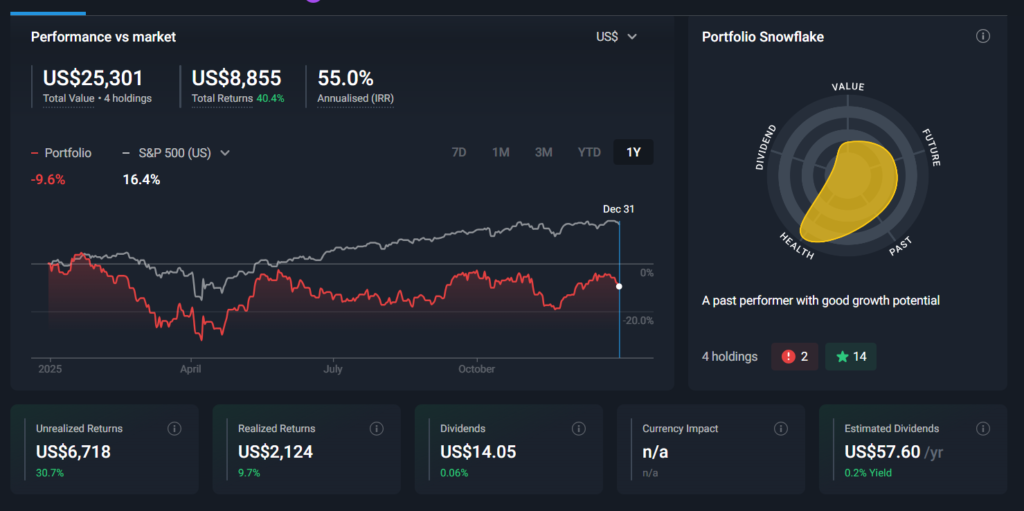

In the year 2025 the portfolio registered a total return of-9.6%, underperforming the broad SP500 benchmark which delivered +16.4% growth over the same period. This performance reflects both challenging macro conditions and idiosyncratic moves in select holdings. The portfolio accumulates a total return of +40.4%.

The portfolio comprised the following equities:

Alphabet (Google)

Bruker Corporation

Fortinet

Tecnoglass

Tesla

Realty Income

Adobe (added during the year)

Key Results & Attribution

Overall Return

2025 Annual Return:−9.6%

Benchmark (S&P 500): +16.4% This gap highlights a period of reallocation and stock-specific volatility rather than broad market exposure.

Cumulative Performance since 2023

Total Return (2024–2025): +40.4%

Major Transactions & Rationale

Bruker Corporation

Liquidated with a realized gain of +51.88%

The position was sold once our internal intrinsic value estimate was breached, allowing redeployment into assets with stronger growth prospects and better risk-reward profiles.

Sale proceeds increased portfolio liquidity and reduced exposure to cyclicality in scientific instruments.

Alphabet (Google)

Realized gain of +21.25%

Traded out earlier in the cycle as price exceeded our fair value estimate, locking in gains. While the stock continued to appreciate, maintaining discipline around valuation was prioritized.

Adobe

New addition in 2025

Introduced based on resilient fundamentals, solid earnings momentum, and strong competitive positioning in digital media/software.

Performance Drivers (Positive & Negative)

Positive Contributors:

Bruker liquidation: Positive realized gains boosted absolute return before reallocations.

Fortinet & Tecnoglass: Continued solid business performance helped mitigate some broader market weakness.

Negative Contributors:

Tesla: High volatility and sector-wide rotation away from growth pressured returns.

Realty Income: Sensitivity to rising rates and real estate sector softness impacted yield-oriented holdings.

Discussion & Context

Risk & Return: The portfolio’s performance must be evaluated in the context of active stock selection and disciplined rebalancing, rather than passive benchmarking. Absolute losses reflect idiosyncratic exposure as well as strategic reallocations in the face of market uncertainty.

Valuation Discipline: Systematically selling positions once they exceed our intrinsic value estimates has supported capital preservation and disciplined reinvestment.

Exposure Review: Allocation shifts during 2025 reflect a bias towards companies with stronger competitive moats and growth visibility.

2026 Priorities

Rebalance Exposure: Consider incremental diversification across sectors and factors (e.g., defensive, value, small caps) to balance growth risk.

Monitor Macro Signals: Rate trends and valuation compression remain critical for equity performance.

Refine Metrics: Incorporate risk-adjusted performance indicators (e.g., Sharpe Ratio) and attribution analysis to better isolate decision impact versus market movements.

Conclusion

While 2025 delivered a negative annual return, performance must be interpreted through the lens of active management and valuation discipline. The portfolio remains positioned to capture growth in selected secular trends, supported by a robust cash position and rigorous valuation frameworks.

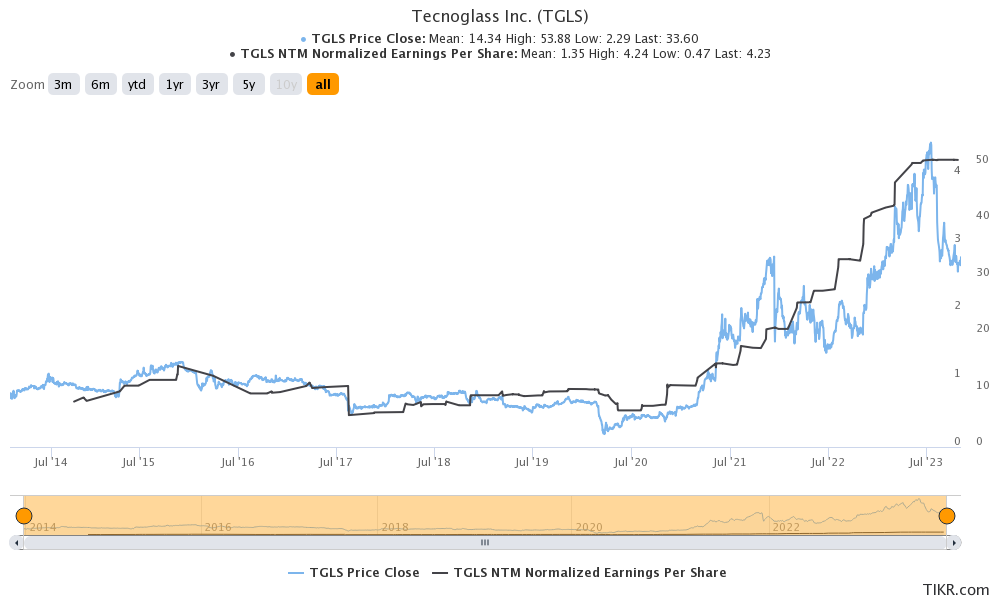

Note: I discovered Tecnoglass around July 2023 when the company was trading at approximately $30 to $35. While the company caught my attention due to the ‘simplicity’ of its business model and its sudden growth from 2021 to 2024, I initially didn’t pay much attention because of its performance trend from 2014 to 2020.

I continued tracking the company and saw a continue increase until 2025, which is when I finally decided to write this full review, and invest on this company.

Introduction

Tecnoglass, Inc. is a leading manufacturer and distributor of architectural glass, windows, and associated aluminum products for both commercial and residential construction markets. The company is headquartered in Barranquilla, Colombia, and operates internationally, with a strong presence in the United States, its largest market.

Source: MarketScreener

It markets and sells its products under the Tecnoglass, ES Windows, and Alutions brands through internal and independent sales representatives, as well as directly to distributors. The company was founded in 1984 and is headquartered in Barranquilla, Colombia. Tecnoglass Inc. is a subsidiary of Energy Holding Corporation.

Key Products and Services:

Architectural Glass

Laminated Glass: Combines multiple glass layers with an interlayer for safety and strength.

Tempered Glass: Heat-treated for durability and thermal resistance.

Insulating Glass: Enhances energy efficiency by reducing heat transfer.

Low-Emissivity (Low-E) Glass: Coated to reflect heat while allowing light.

2. Windows and Aluminum Products:

Windows and Door Systems: Designed for aesthetic appeal, energy efficiency, and impact resistance.

Curtain Walls: Exterior cladding systems for large-scale commercial buildings.

Storefront Systems: Glass systems for retail and commercial applications.

3. Specialty Products:

Impact-Resistant Glass: Built to withstand severe weather conditions and meet hurricane safety standards.

Custom Solutions: Tailored products for unique architectural designs and client needs.

Tecnoglass primarily serves the construction sector, catering to High-rise commercial buildings, Residential properties, including luxury homes and Infrastructure projects.

Competitive Advantages:

1. Vertical Integration: Tecnoglass owns and operates its manufacturing facilities, ensuring strict quality control, cost efficiency, and faster turnaround times.

2. U.S. Market Leadership: The company has a strong distribution network in the U.S., with significant market share in the Southeastern and Southwestern regions.

3. Innovation and Sustainability: Tecnoglass emphasizes energy-efficient and environmentally friendly products, aligning with growing demand for sustainable construction materials.

The main competitors of Tecnoglass are PGT Innovations, Inc. (PGTI), Apogee Enterprises, Inc, (APOG), and Cardinal Glass Industries (which is a private company) and these companies are part of the Industrial sector.

Market Growth

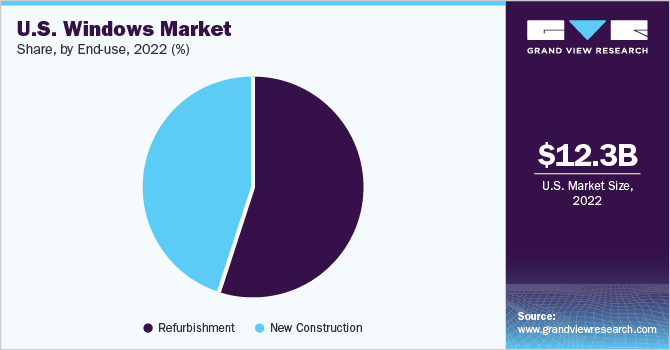

Source: Grand View Research, 2024

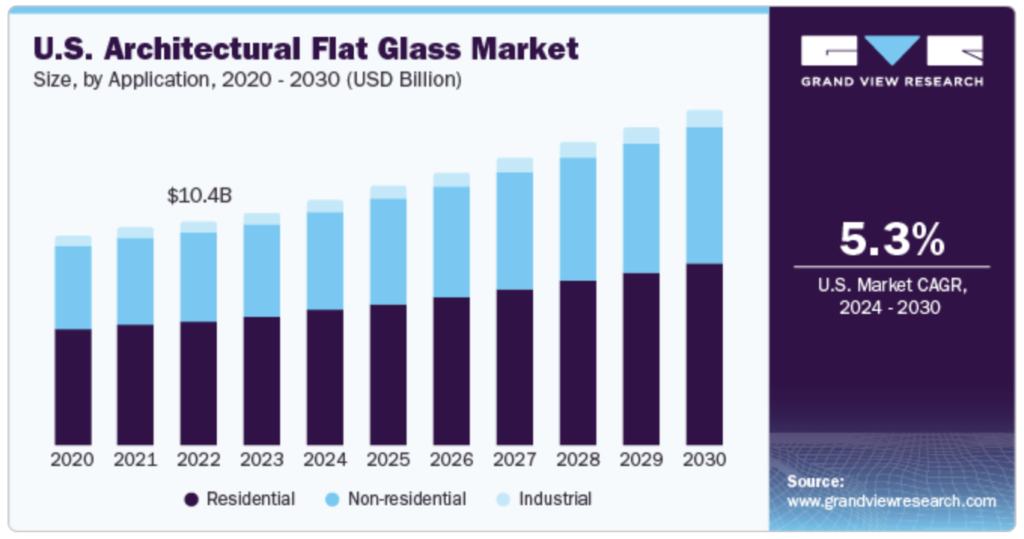

In the United States, the architectural glass market is expected to grow at a higher CAGR of 4.9%, from USD 572 million in 2023 to USD 802 million by 2030, supported by strong renovation activity and premium demand for low-E and impact-resistant products.

Other research firms show similar yet slightly more conservative trajectories. MarketResearch.com projects global architectural glass to grow from USD 219 billion in 2023 to USD 258 billion by 2030, corresponding to a ~2.8% CAGR. Meanwhile, when the broader flat glass market (including automotive and solar applications) is considered, Grand View Research forecasts USD 311 billion in 2024 rising to USD 405 billion by 2030, a 4.6% CAGR, confirming the medium-term resilience of the category.

Source: Grand View Research – US Windows Market

Key Risks and short-term headwinds

While the long-term outlook remains favorable, several short-term risks could weigh on demand. The macroeconomic environment — especially high mortgage rates in the U.S. — has already begun to slow home improvement spending. A recent Financial Times article noted that homeowners are postponing major upgrades due to financing costs.

The Fenestration & Glazing Industry Alliance (FGIA) reported in 2024 that new-construction window demand grew ~1%, but replacement window demand fell ~5%, with another mild decline expected in 2025 before a rebound in 2026–2027 (FGIA Industry Review 2024).

Beyond macro factors, input-cost volatility (aluminum, PVC, logistics) and trade tariffs represent recurring threats to margins. Competitive pressure is also intensifying, as large incumbents (JELD-WEN, Andersen, Pella) streamline operations and pursue share in vinyl and energy-efficient categories.

Q2 2025, Consistency and Execution at record levels

Tecnoglass delivered another record quarter in Q2 2025, proving once again that operational excellence and disciplined capital allocation can outperform cyclical headwinds in construction.

Revenue hit an all-time high of $255.5M, up 16.3% YoY, with Adjusted EBITDA of $79.8M (+24.5% YoY) and margins expanding 200 bps to 31.2%. Gross margin improved to 44.7%, benefiting from stronger retail pricing, operational leverage, and a favorable FX tailwind as the Colombian peso weakened 7% versus the USD.

The company’s backlog reached a record $1.2B (+17% YoY) — 97% based in the U.S. — ensuring visibility well into 2026. The book-to-build ratio of 1.2x underscores sustained demand across multifamily and commercial projects, especially in high-end condos and luxury lodging where interest-rate sensitivity is lower.

On the residential side, single-family revenues grew 14.5% YoY to $109.6M, driven by expanding dealership networks, new showrooms, and strong traction in vinyl windows — a move that more than doubles Tecnoglass’ addressable market. Orders rose 29% sequentially, marking the second-highest quarter on record and reinforcing growth momentum into the second half of the year.

From a financial standpoint, Tecnoglass remains exceptionally strong:

Net cash position: $28.7M

Liquidity: ~$310M

Net debt/EBITDA: –0.09x (no leverage)

ROE (3yr avg): 39% vs 16% peers

ROIC (3yr avg): 27% vs 10% peers

The company’s vertically integrated model — from glass manufacturing to installation — continues to be its structural moat, enabling industry-leading lead times (5–6 weeks) and resilient margins despite aluminum tariffs and labor inflation.

For 2025, management expects revenue between $980M–$1.02B and Adjusted EBITDA of $310M–$325M, with gross margins in the low-to-high 40% range. Even under conservative assumptions, Tecnoglass is positioned to sustain superior returns on capital and compound value over time.

Assessing the Upsides and Downsides of Tecnoglass: My Perspective

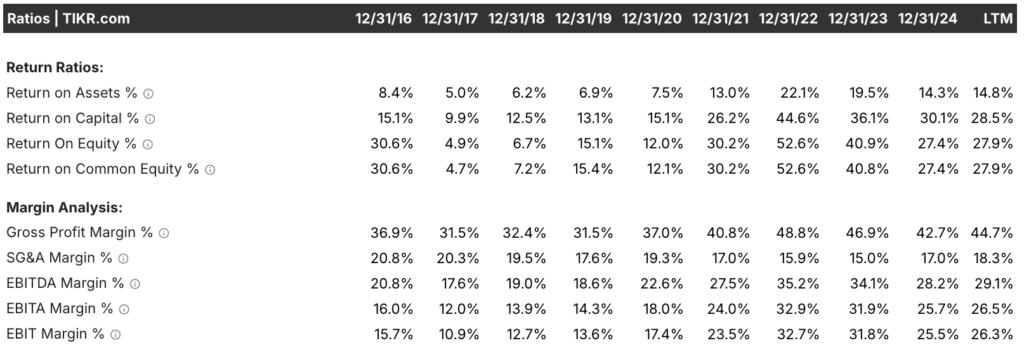

Tecnoglass has structurally upgraded its profitability profile. While 2021–2022 benefited from an exceptional demand cycle, the company’s normalized returns (25–30% ROE, ~28% ROC) suggest it retained most of those efficiency gains. This is consistent with a business that achieved scale, pricing power, and cost control — all signals of a growing economic moat.

Source: Tikr, Return Ratios and Margin Analysis

The margin expansion is structural, not cyclical. It results from (1) vertical integration, (2) efficiency in SG&A scaling, (3) dominance in U.S. distribution, and (4) product mix evolution (more premium vinyl and impact-resistant products). The slight decline in 2023–2024 simply reflects normalization from extraordinary highs, not deterioration in fundamentals.

The sustained ROE >25% and EBITDA margins near 30% suggest a competitive advantage that goes beyond a short-term cycle. The moat appears to rest on three pillars:

Vertical Integration: Tecnoglass controls the entire value chain — from glass manufacturing to aluminum framing and installation — ensuring cost control, faster delivery, and superior margins.

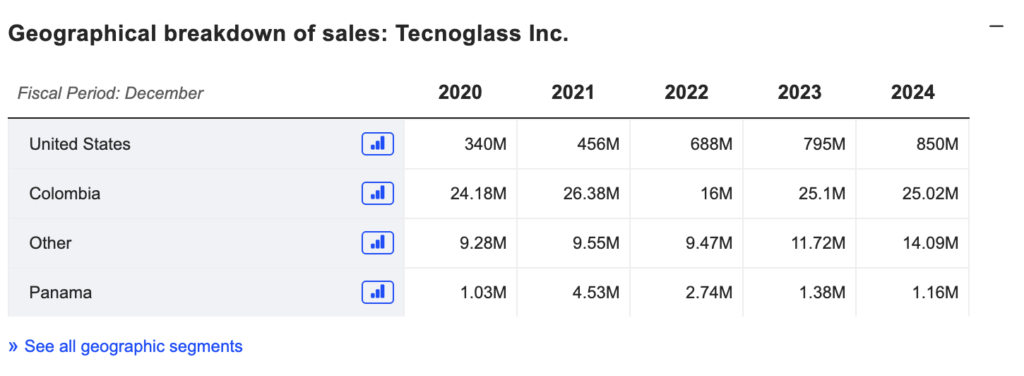

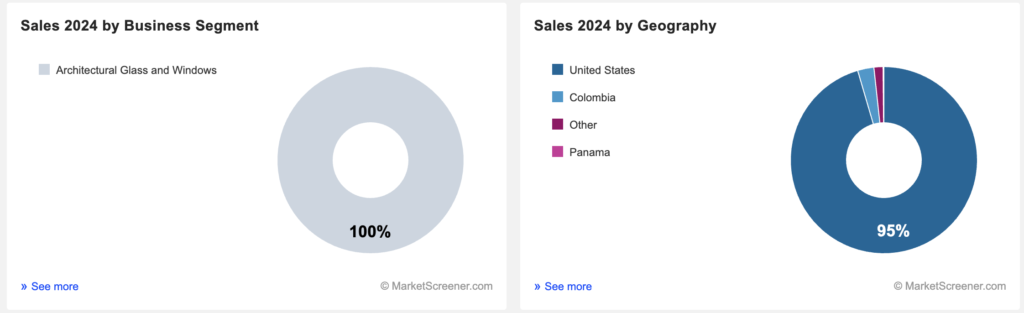

Geographic Focus: 95% of revenue now comes from the U.S., particularly Florida and the Sun Belt, where code requirements (impact resistance, hurricane glazing) favor high-spec products.

Operational Efficiency: The company’s production hub in Barranquilla offers structural cost advantages (labor, logistics, tax incentives) versus U.S. peers like Andersen or JELD-WEN.

These factors explain why margins remain high even as demand normalizes. In essence, Tecnoglass behaves less like a commodity manufacturer and more like a specialized premium supplier with pricing power and economies of scale.

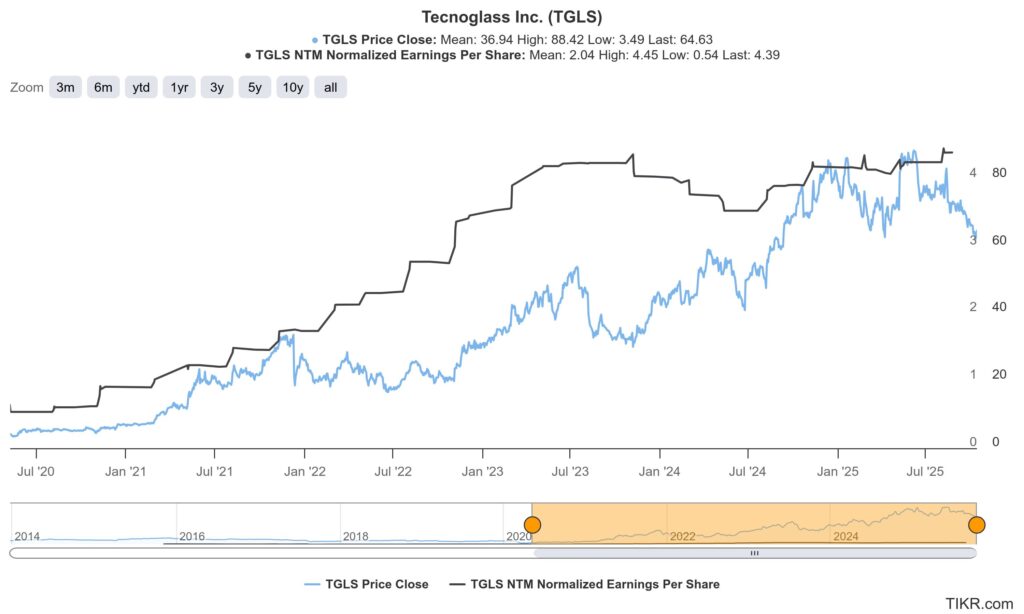

Inefficiencies between the price and its capacity to generate value, EPS has been growing since 2020, and the company is still reporting high earnings per share, but the price tanked in Jul 2023.

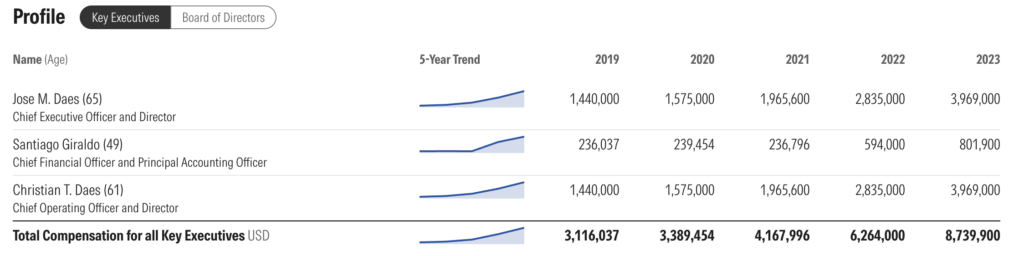

Leadership Analysis

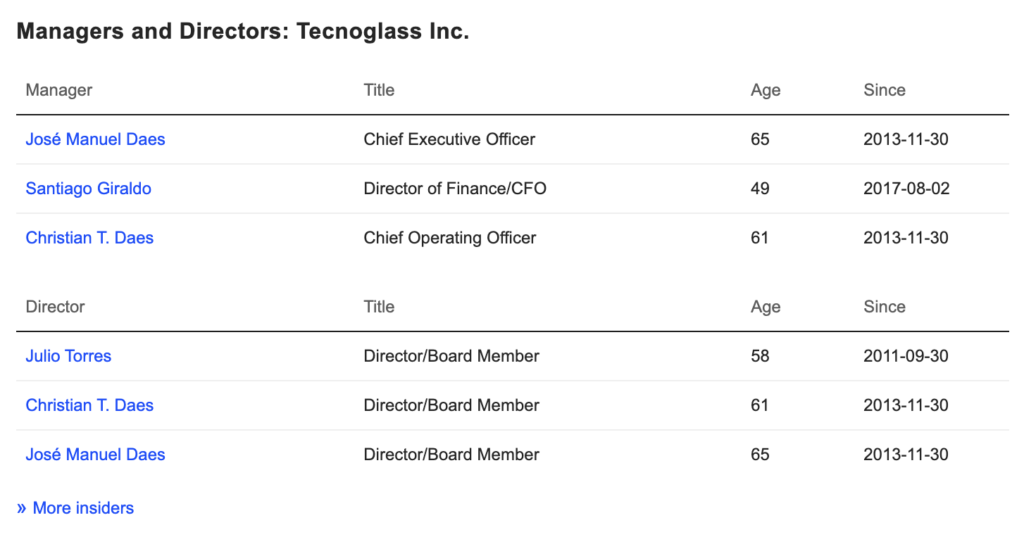

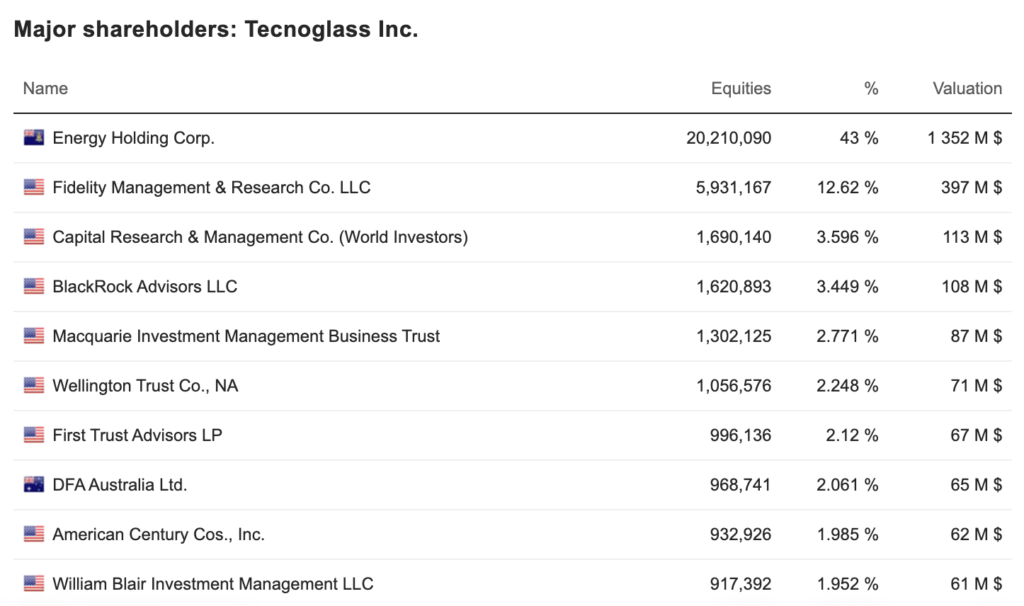

Tecnoglass was founded in 1984 in Barranquilla, Colombia, by the brothers José M. Daes and Christian T. Daes, and it was a family-owned business from the start. The company made its debut on the U.S. stock exchange through a business combination in 2013 and later moved its listing to the NYSE. However, the Daes family still holds a significant stake, primarily through Energy Holding Corporation. This entity owns roughly 43% of the outstanding shares (according to recent filings), which is a positive sign. Not only does it show that the founders, who serve as CEO and COO, maintain a key role, but the family retaining a large share conveys a strong alignment between their interests and the company’s long-term success.

Source: MarketScreener, Managers and Directors.Source: Morningstar – Executive Team Yearly Compensation

The main reason why the owners of Energy Holding Corp are also the owners of Tecnoglass is because Energy Holding Corporation (EHC) is the entity through which the founding family of Tecnoglass, brothers José M. Daes and Christian T. Daes, maintain their majority stake in the publicly traded company.

Essentially, it is not that Energy Holding Corp owns Tecnoglass in a traditional “energy holding” manner, but rather that:

1.- José M. Daes (CEO and Director) and Christian T. Daes (COO and Director) are the founders of Tecnoglass.

2.- They and their family members are the indirect owners of Energy Holding Corporation (EHC).

3.- EHC is, in turn, the largest shareholder of Tecnoglass Inc., a company listed on the stock exchange (NASDAQ and/or NYSE, historically).

The ownership structure through Energy Holding Corporation generally serves a strategy of:

By consolidating their shareholding through a single entity (EHC), the Daes family can maintain significant voting control over the decisions of the board of directors and the strategic direction of Tecnoglass, even though the company is publicly traded and has other institutional and minority shareholders. This allows them to drive their long-term vision for the company.

Capital and Liquidity Management:

Company Financing: Initially, this structure enabled the creation and growth of the company.

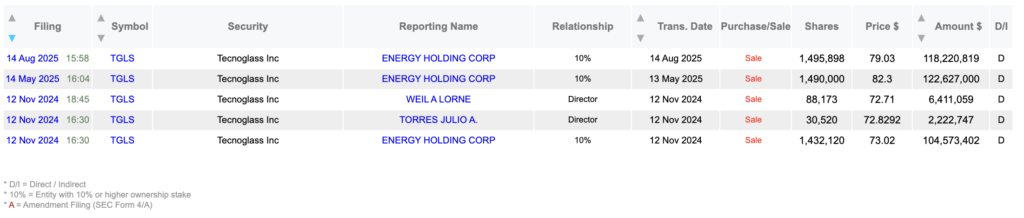

Secondary Sales: Energy Holding Corp has made secondary offerings of shares (block sales) in the past. This is a way for the founding owners to obtain liquidity (cash) from their investment without Tecnoglass itself issuing new shares and diluting all other shareholders. They are simply selling a portion of their consolidated stake to the market.

Dara Roma – Insidels Sells 2024 – 2025

We have not identified unexpected movements or aggressive sales from the Executive team or board of Directors.

Financials

Income Statement

Accordin to the company: During the third quarter, the Company returned capital to shareholders through an aggregate of $30.0 million in share repurchases and $7.0 million in cash dividends.

In November 2025, the Company’s Board of Directors authorized the expansion of the Company’s share repurchase authorization to $150.0 million to execute during opportunistic times.

Management will have discretion in the repurchase of common shares, including the timing and amount to be repurchased. Following the expansion, the Company had approximately $96.5 million remaining under its existing share repurchase program.

Q3 2025 Results heavily impacts the stock price.

Following the Q3 results, I summarised the biggest insights in the following bullet points:

Strong liquidity: ~US$550 million total liquidity including cash (~US$124 m) + credit facility (~US$425 m) with debt of US$111.9 m. investors.tecnoglass.com

Expansion of buy-back: US$30 m share repurchase in Q3 + dividend US$7 m; and share repurchase program expanded to US$150 m. investors.tecnoglass.com

Guidance updated: Full-Year 2025 revenue range revised to US$970-990 m and Adjusted EBITDA to US$294-304 m. investors.tecnoglass.com

On the surface, many things are going well: revenue growth, backlog growth, strong liquidity, shareholder capital returns, and improved strategic positioning. These are positive signals typically associated with a high-quality, possibly compounder business.

But, despite the strong headline, there are a number of caveats in the release and surrounding commentary that likely dampened investor enthusiasm:

Adjusted EBITDA margin dropped to ~30.4% from ~34.2% the year ago quarter. investors.tecnoglass.com

Management explicitly flags “higher raw material cost related to all-time high premiums for U.S. aluminium, and a revaluation of the Colombian Peso” as drivers. investors.tecnoglass.com Interpretation: While growth is positive, margins are under pressure. For a business whose investment case hinged partly on margin expansion, any margin erosion triggers concern.

Single-family residential growth moderating

Single-family residential revenues grew only 3.4% YoY compared to the higher growth in multi-family/commercial (14.3%). investors.tecnoglass.com Interpretation: Since the single-family market is more sensitive to interest-rates, housing cycles, and consumer sentiment, the low single-family growth suggests some vulnerability.

Unfavourable revenue mix: higher installation content (which tends to carry lower margins than product sales) is cited. investors.tecnoglass.com Interpretation: These factors imply that underlying margins might be under pressure beyond just cost inflation — mix and FX are structural headwinds.

Guidance seems conservative / lower than previously expected

While management raised full-year guidance, the ranges (US$970-990 m revenue, US$294-304 m EBITDA) reflect only ~10% revenue growth and ~8% EBITDA growth at midpoint. investors.tecnoglass.com

Some commentary from market watchers noted that the company “missed consensus expectations” despite the growth. Finimize+1 Interpretation: Investors often like not just growth, but upside surprise and margin improvement. When the guidance is conservative and margins contract, sentiment can turn even if absolute results are good.

Valuation reset / analyst target cuts

Analysts have lowered price targets (e.g., DA Davidson cut TGLS target from ~US$95 to ~US$80. GuruFocus

The stock hit new 52-week low despite results. MarketBeat Interpretation: Analyst target reductions and technical breakdowns often trigger negative momentum. Even a good business can suffer share price weakness if growth/margin expectations are lowered.

Why has the share price dropped to below ~$50? (Putting it all together)

Bringing the above points into a cohesive narrative:

Even though growth is positive, the margin contraction and cost/mix/FX headwinds suggest that the “best-case” scenario (continuous margin expansion) may be under threat. For a stock that previously traded on high return metrics and margin improvement, this is a material shift.

The single‐family residential slowdown, in a business where that segment is meaningful, introduces cyclical risk — fear of interest‐rate pressure, housing market softness, and renovation hesitancy.

The guidance, while positive, is not aggressive; investors may have been expecting more upside or margin improvement rather than stability. The fact that it reflects only ~8% EBITDA growth (in a business that previously delivered much higher growth) may disappoint.

Analysts and the market are re-pricing the risk: margin pressures + cyclical exposure + cost inflation = higher risk premium. So the valuation multiple is compressing.

Technical and sentiment factors: hitting a 52-week low often spurs investor caution; when analysts cut targets, this can become a self-reinforcing negative spiral (sell side lowers target → investors sell → share price falls → more negative sentiment).

The business remains fundamentally strong, but the “promise” of continued margin expansion and high growth might be being recalibrated; investors sometimes rotate out before the new metrics embed.

Valuation

Source: In–houseproduction – Intrinsic Value Calculation.

The analysis shows that the current share price of TGLS is $46.55, while the calculated intrinsic value is approximately $78.71, with a 30% a margin of safety, it will recommend a purchase price at $55.10.

Source: In–houseproduction – Price Evolution based on P/E Ratio.

Based on the analysis performed, I consider TGLS to be undervalued in terms of its intrinsic value, given that the current share price is below its calculated value. scena

However, it is essential to note that growth projections are optimistic and may not materialize. The company shows a solid return on capital and good growth potential, but investors should be cautious about expectations.

BRKR or Bruker Corporation is a leading manufacturer of scientific instruments that are used by customers in life sciences, pharmaceuticals, applied markets, and academia. The company also provides diagnostic tools for microbiology and pathology labs.

Introduction

Bruker Corporation’s offerings can be categorized into the following segments:

Bruker BioSpin Group: This segment offers products like nuclear magnetic resonance (NMR) spectrometers, magnetic resonance imaging (MRI) systems, and preclinical MRI research tools. They also provide solutions for EPR (electron paramagnetic resonance) applications.

Bruker CALID Group: The CALID group offers a wide range of products including mass spectrometry tools, microbiology and diagnostic tools, infrared spectroscopy systems, and gas chromatography systems.

Bruker Nano Group: This segment offers advanced materials research tools, nanoanalysis solutions, and microscopy, all of which are used in the semiconductor and other industrial markets.

After-Sales Service: Apart from the primary products, Bruker also offers after-sales services including training, preventive maintenance, and other support services.

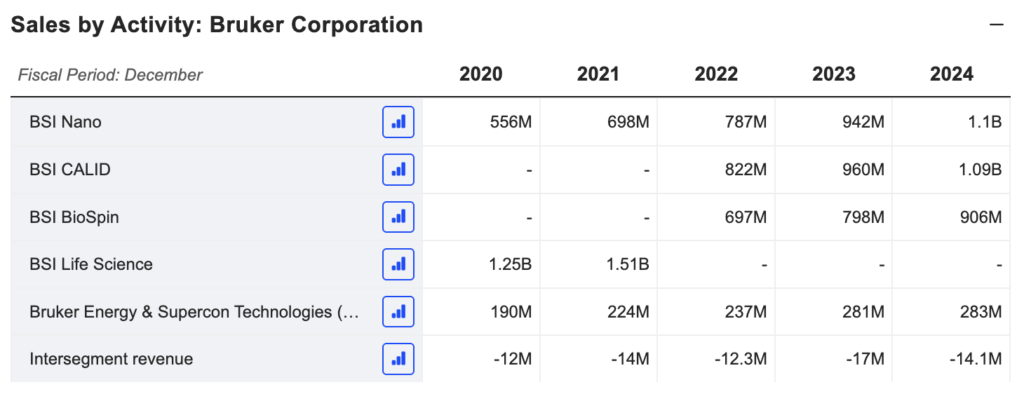

Their main lines of business include the design, manufacture, and distribution of high-performance scientific instruments and analytical and diagnostic solutions. Bruker operates in two segments: Bruker Scientific Instruments (BSI) and Bruker Energy & Supercon Technologies (BEST).

Source: Market Screener – Sales by Activity: Bruker Corporation

BSI encompasses the Bruker BioSpin Group, the Bruker CALID Group (which includes the Bruker Chemical & Applied Markets division, the Bruker Detection division, and the Bruker Daltonics division), and the Bruker Nano Group. These groups focus on advanced analytical solutions for the life sciences and physical sciences research, pharmaceuticals, biotechnology, and industrial markets.

The BEST segment designs, manufactures, and distributes superconducting materials, primarily metallic low temperature superconductors, for use in magnetic resonance imaging, nuclear magnetic resonance, fusion energy research, and other applications.

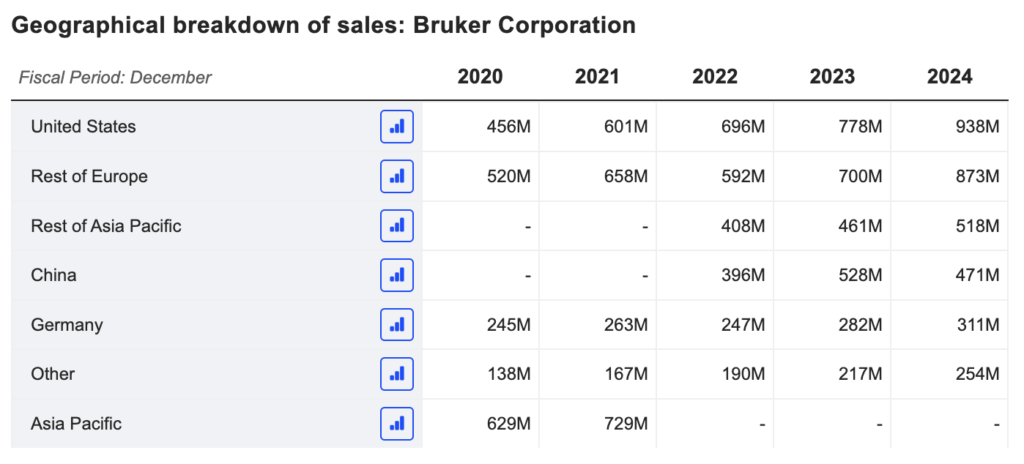

Bruker Corporation operates globally, with customers in over 60 countries. They have major operations in Europe and North America, with presence in Asia, Australia, and the Middle East. They have numerous sales and service offices around the world, including in the United States, Germany, United Kingdom, France, Japan, China, South Korea, India, and Australia. Their corporate headquarters is located in Billerica, Massachusetts, USA.

Source: Market Screener – Geographical breakdown of sales: Bruker Corporation

How does the company make money? Bruker Corporation generates revenue through the following streams:

Sale of Scientific Instruments: Bruker designs, manufactures, and distributes a broad range of proprietary life science and materials research systems and associated products. Their instruments are sold to customers in the pharmaceutical, biotechnology, and molecular diagnostic industries as well as to academic research institutions.

Aftermarket Sales and Services: After the initial sale of an instrument, Bruker continues to generate revenue through the sale of consumables, accessories, software, and services related to their products. This includes maintenance contracts, repair services, training, and consulting.

Collaborations and Partnerships: The company also enters into strategic partnerships and collaborations with other companies and research institutions. These collaborations may generate revenue through licensing fees, milestone payments, and royalties.

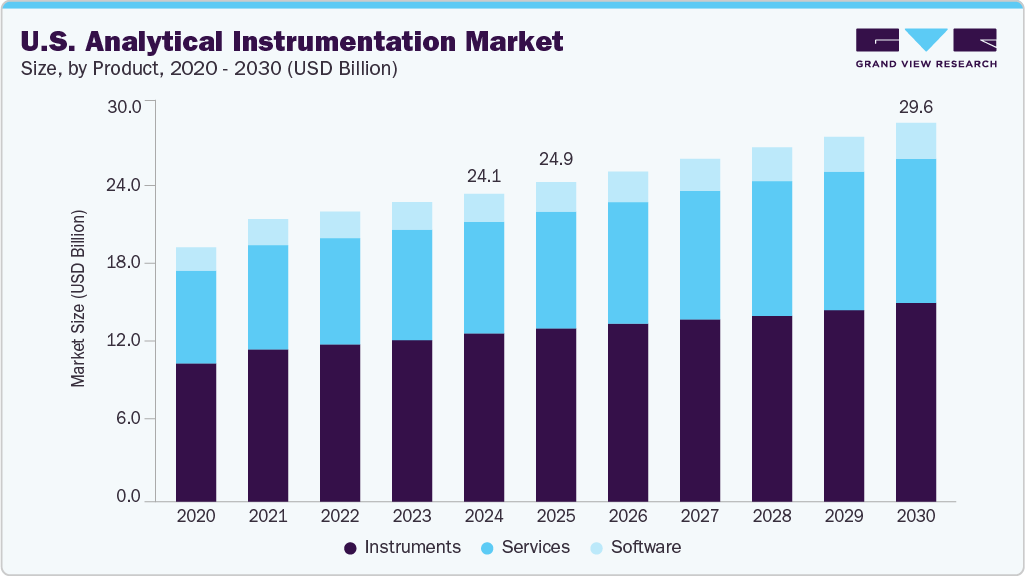

The global Analytical Instrumentation market is projected to grow to USD 76.87 Billion, and only in the US, it has been been growing since 2020, especially in North America, Europe, and Asia Pacific.

Regionally, North America commands the largest share—between 35% and 47% of global revenue in 2024. The U.S. market alone generated around USD 23.4 billion in 2024 and is expected to grow at a 5.5% CAGR to USD 37.7 billion by 2033. Meanwhile, Asia-Pacific, with a 2024 base of approximately USD 11.2 billion, is the fastest-growing region, with forecasts projecting a 7.2% CAGR through 2033 (reaching USD 20.6 billion)

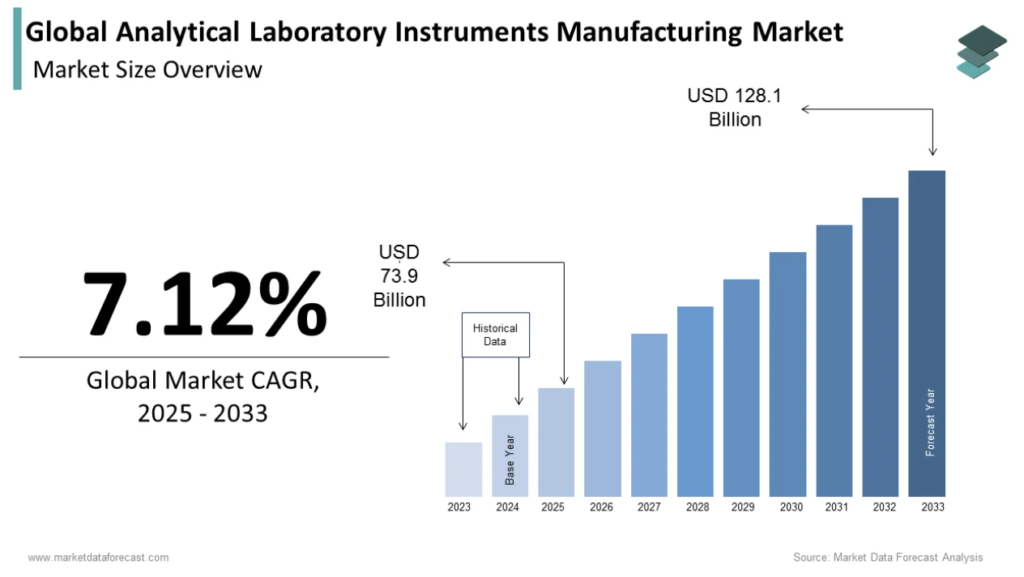

Several market reports estimate a CAGR for the global scientific instrument market ranging from 4.7% to 11.5% until 2030, depending on the specific segment (e.g., process spectroscopy).

Source: https://www.marketdataforecast.com/

Bruker Corporation (BRKR) Outlook

Bruker is well-positioned to benefit from this sector growth, although it faces its own challenges:

Growth Projections: Analysts anticipate that Bruker Corporation will have annual revenue growth exceeding 3% and double-digit EPS growth in the coming years.

Market Position: The company benefits from its diversified product portfolio and strategic acquisitions, which allow it to capitalize on opportunities in high-growth markets such as proteomics and spatial biology.

Risks: Despite the positive outlook, the company faces risks such as the volatility of its profit margins, dependence on R&D investment (which can be fluctuating), and strong market competition.

Bruker’s Growth vs. its Rivals Revenue Performance: Bruker has achieved consistent revenue growth. In fiscal year 2024, it reported an organic revenue growth of 4.0%, and for the first quarter of 2025, the organic growth of its scientific instruments segment (BSI) was 5.1%.

Market Share Performance

Despite intense competition, Bruker has proven capable of gaining market share in key areas such as mass spectrometry, molecular diagnostics, and spatial biology, often through strategic acquisitions. Bruker Corporation has currently a 8% in the Laboratory Analytical Instruments.

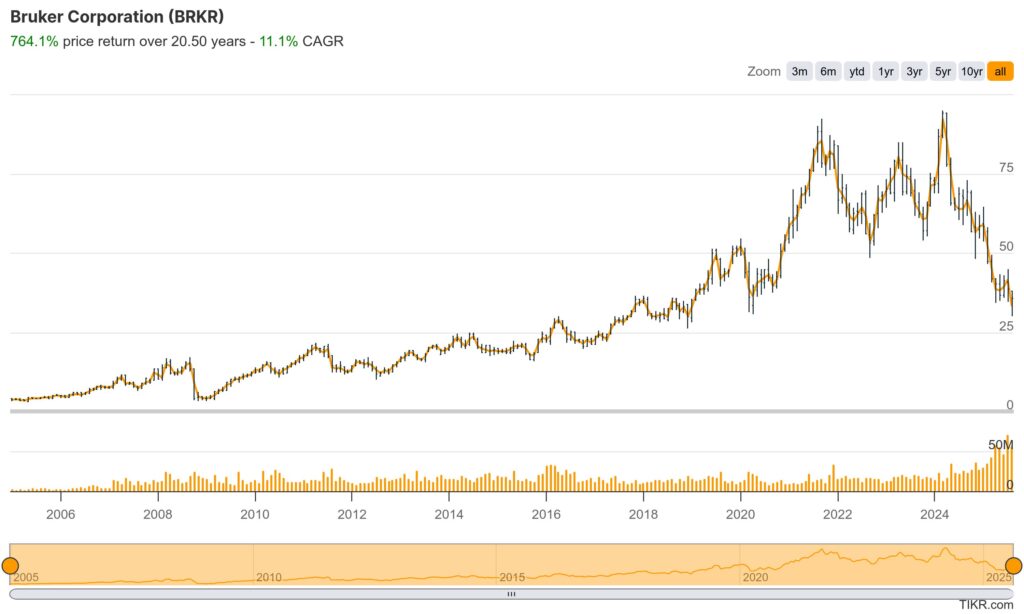

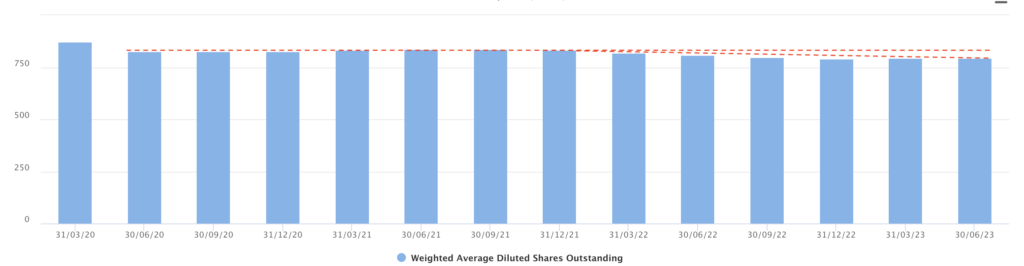

Stock Shares Decreases during H1 by >50%

Source: TIKR – Stock Price

Who hasn’t had a rough day? Well, in this case, it’s more like a rocky start to the year. But let’s see just how ‘bad’ it really has been, maybe it’s not so terrible after all!

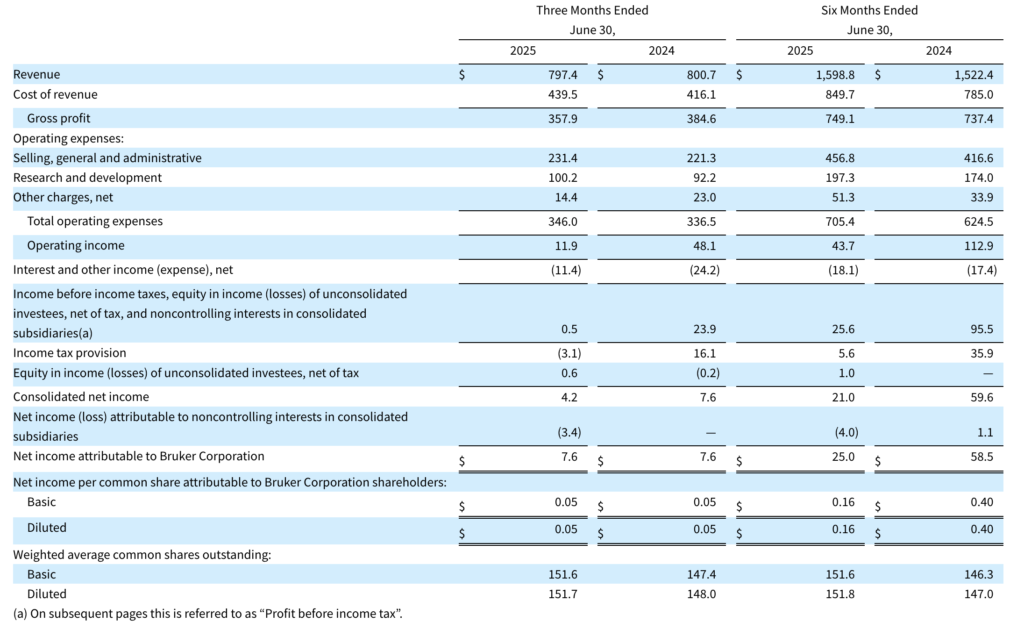

In Q1 2025, Bruker reported revenues of $801.4 million, up 11% year-over-year, driven by strong demand in biomedical research and protein analysis. GAAP EPS was $0.11, down 68.6%, but non-GAAP EPS reached $0.47, exceeding expectations. The non-GAAP operating margin was 12.7%, and operating cash flow stood at $57.1 million, reflecting solid operational efficiency. The company maintained a net cash position of $1.93 billion and continued investing in post-genomic biology and drug discovery, supporting long-term growth.

In Q2 2025, revenues slightly declined to $797.4 million, down 0.4% year-over-year, with organic revenue falling 7% and constant-currency revenue down 3.3%. GAAP EPS dropped to $0.05, while non-GAAP EPS fell to $0.32, reflecting weaker demand in the academic and U.S. biopharma markets.

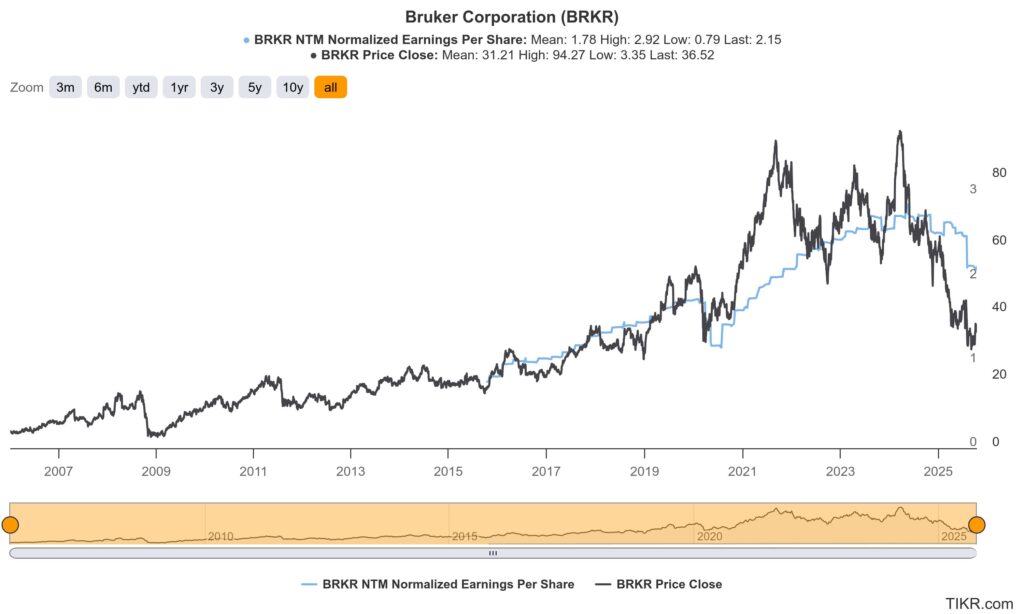

Source: Bruker Reports Second Quarter 2025 Financial ResultsSource: TIKR, NTM Normalized EPS and Price.

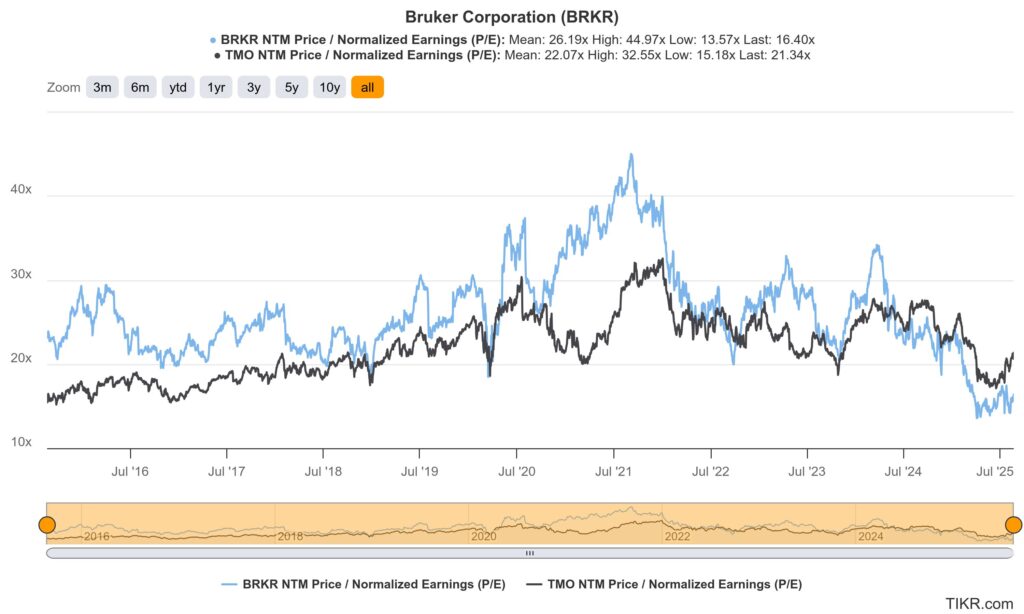

From a value perspective, the long-term price action for Bruker Corporation (BRKR) has exhibited a significant concern, particularly in the period from 2020 to 2024. During this time, the BRKR Price Close dramatically outpaced its fundamentals, showing an extreme divergence from the NTM Normalized EPS trend. This suggests the stock was trading at highly inflated multiples, disconnected from its underlying earnings power and relying heavily on speculative growth assumptions. As of late 2024 and 2025, the market has executed a sharp correction, significantly eroding the share price and closing the historical valuation gap. While this deleveraging of the multiple brings the price closer to a rational level—validating the view that the stock was previously overvalued—investors must now assess whether the current valuation offers a genuine margin of safety or if further earnings deceleration has been priced in.

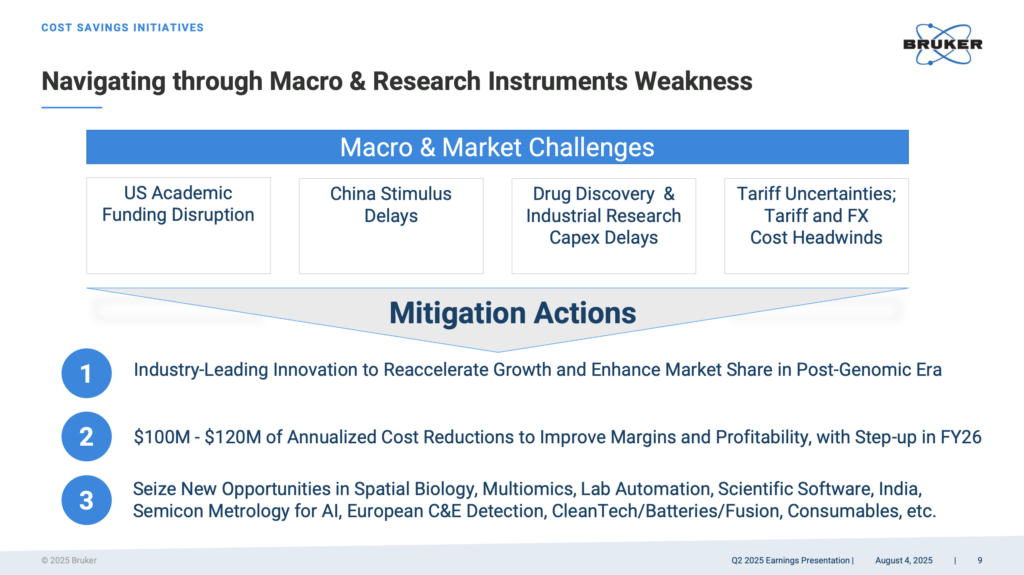

CEO Frank Laukien during the earnings call, described the quarter as “challenging,” attributing the underperformance to reduced demand in the U.S. academic sector, as well as in biopharma and industrial markets. Additionally, global tariffs and currency headwinds further impacted the company’s performance. To address this, Bruker launched cost-saving initiatives targeting $100–$120 million in annual reductions by 2026, as well Despite near-term challenges, continued investment in innovation positions the company for sustainable growth.

Source: Q2 2025 Earnings Presentation

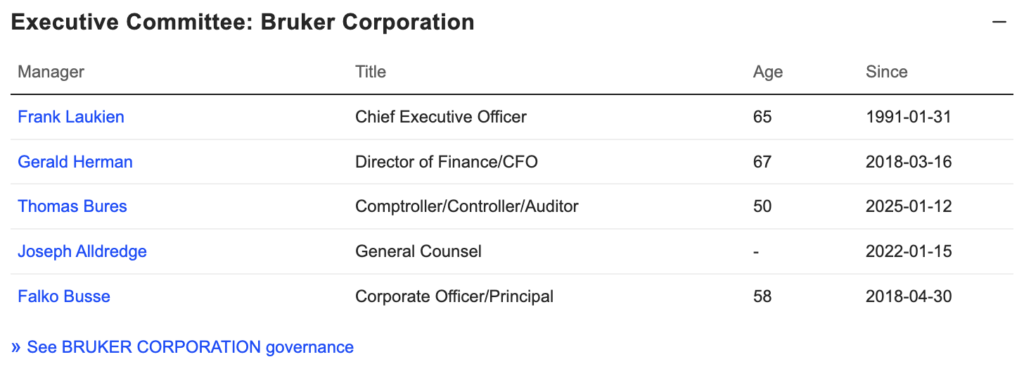

Leadership Team Analysis

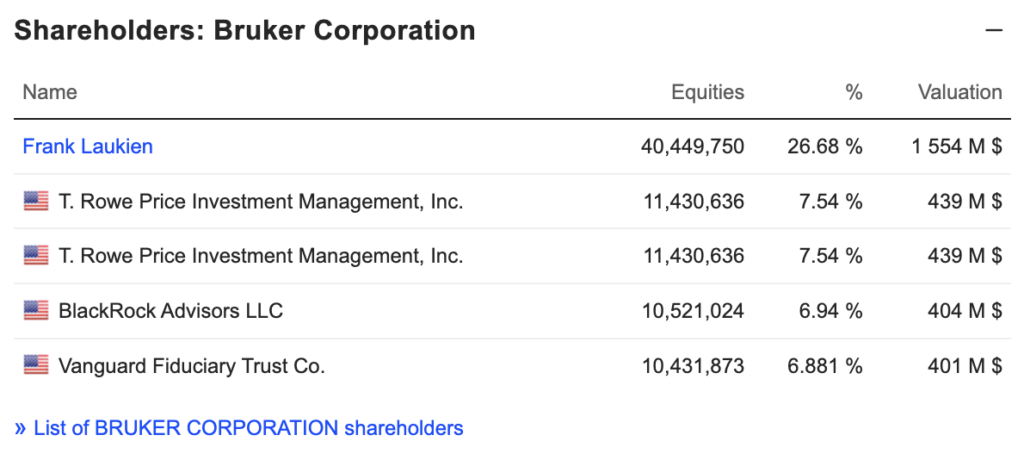

The company was founded in 1960 by Gunther Laukien in Karlsruhe, Germany, and initially, it was a family-owned business. However, it went public in 2000. Burker’s CEO Frank Laukien, holds more than 40M shares (26.68% of shares outstanding held), which is a good sign not only because he has a key role in the company but also because the Laukien family keeps a big share of the company, and convey a solid alignment between their and the company’s interests.

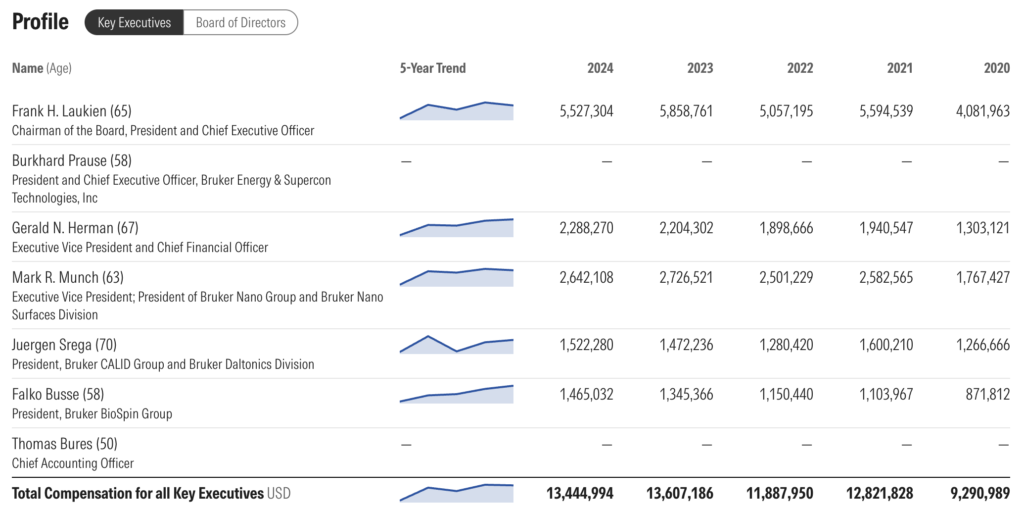

Below, I’ve included a snapshot of Bruker’s Key Executives, along with their yearly compensation. None of the stakeholders makes more than 10% in revenue, which is a positive sign and it makes me feel that the leadership team is not squeezing the organization funds.

Source: Morningstar – Executive Team Yearly Compensation

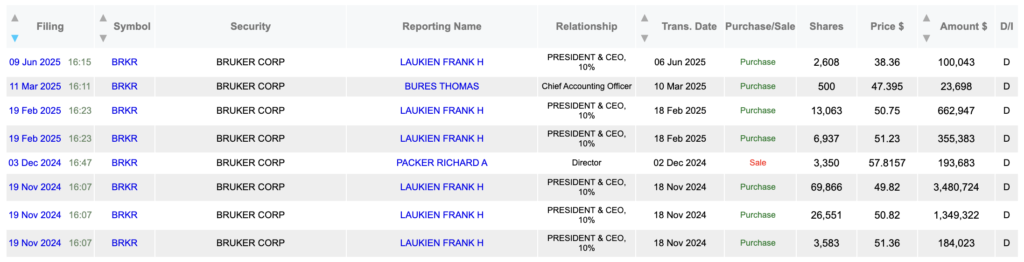

Regarding the Insiders, we have not identified unexpected movements or aggressive sales from the Executive team or board of Directors. In fact, the CEO has being buying since Q1 2025.

Data Roma – Insiders

4.- Competitive advantages As one of the top five players (alongside Agilent, Thermo Fisher, Shimadzu, Danaher), it captures a significant share of the consolidated analytical instrumentation market (approx. 65% combined share among these players, according to Mordon Inteligence).

The company’s strength lies in its expertise in mass spectrometry, material research, molecular analysis, and spectroscopy—areas aligned with the fastest-growing product categories. Innovations like timsTOF Ultra, Orbitrap, and high-resolution MS platforms place Bruker at the forefront when it comes to sensitivity, throughput, and advanced analytics, meeting laboratory needs in proteomics, complex mixtures, pharmacological pipelines, and emerging sectors like battery materials. Customers rely heavily on vendor service support, often through tiered maintenance contracts—an area where Bruker has robust capabilities.

Regionally, Bruker is well-positioned to capitalize on growth in North America (largest market) and Asia-Pacific (fastest CAGR). Its global footprint and integration of automation, remote analytics, and AI-enable tools further differentiate it—especially as labs modernize workflows and seek predictive maintenance, cloud connectivity, and higher throughput.

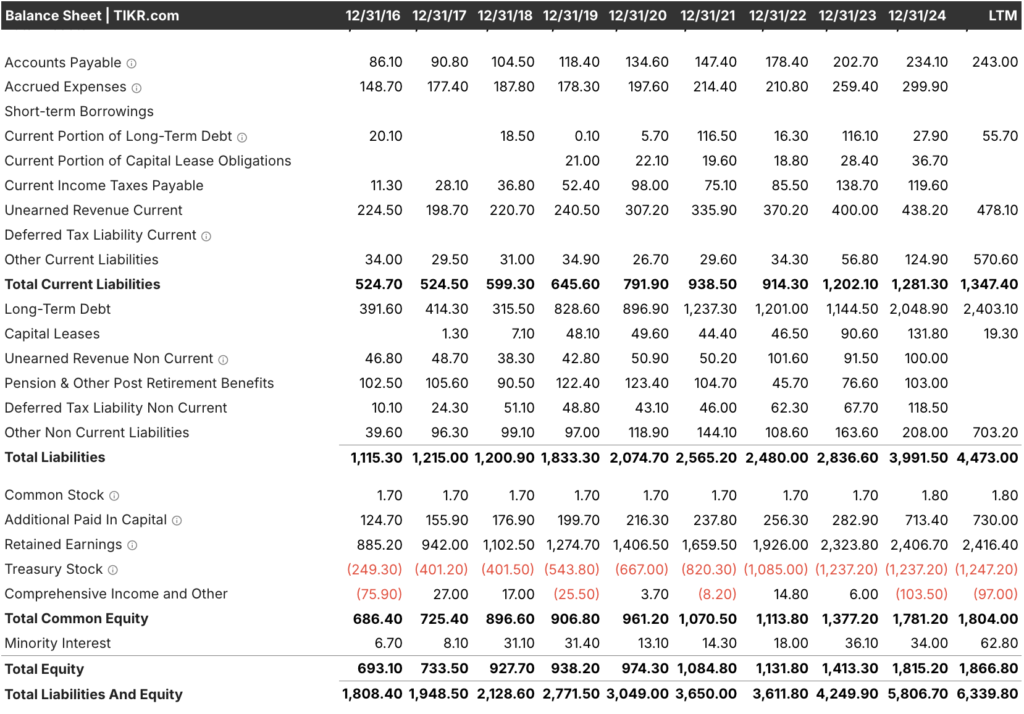

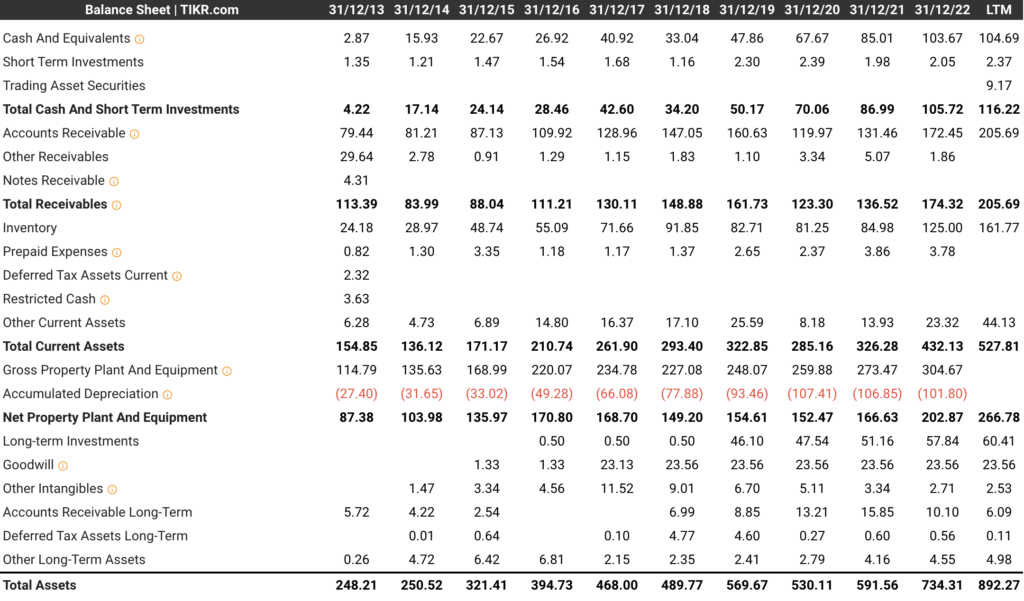

The company has good short-term liquidity ratios, especially the Current Ratio (total current assets / total current liabilities) which has been above 1 since 2013 and explains its power to pay down the current liabilities. It’s important to mention that the Current Ratio has decreased over the last three years, which is a metric that should be monitored to ensure the company keeps strong.

Switching Cost

Bruker’s customers face significant switching costs due to the high capital investment and specialized nature of its instruments. For instance, the average price of a Bruker mass spectrometer is approximately $500,000, with installation and training adding an additional 20% to the total cost. This substantial investment creates a high barrier to switching, as laboratories would incur significant costs to replace or retrofit equipment from another vendor.

Additionally, Bruker’s instruments are often integrated into complex workflows that include proprietary software and consumables. This integration further increases the switching cost, as transitioning to a new system would require not only replacing the hardware but also retraining staff and adapting existing processes. Such comprehensive changes are time-consuming and costly, reinforcing customer loyalty and reducing turnover.

Training Cost

Operating Bruker’s advanced instruments requires specialized knowledge, leading to substantial training costs. Training programs are typically conducted by Bruker-certified instructors and can last several weeks, depending on the complexity of the equipment. For example, training for a high-end NMR system can cost upwards of $10,000 per participant Wikipedia. These costs are often borne by the customer, adding to the overall expense of adopting Bruker’s technology.

Moreover, Bruker frequently updates its software and hardware, necessitating ongoing training to ensure users remain proficient. This continuous need for education creates a long-term commitment for customers, as they must allocate resources for periodic training sessions to keep pace with technological advancements.

Financials

Income Statement detailed review

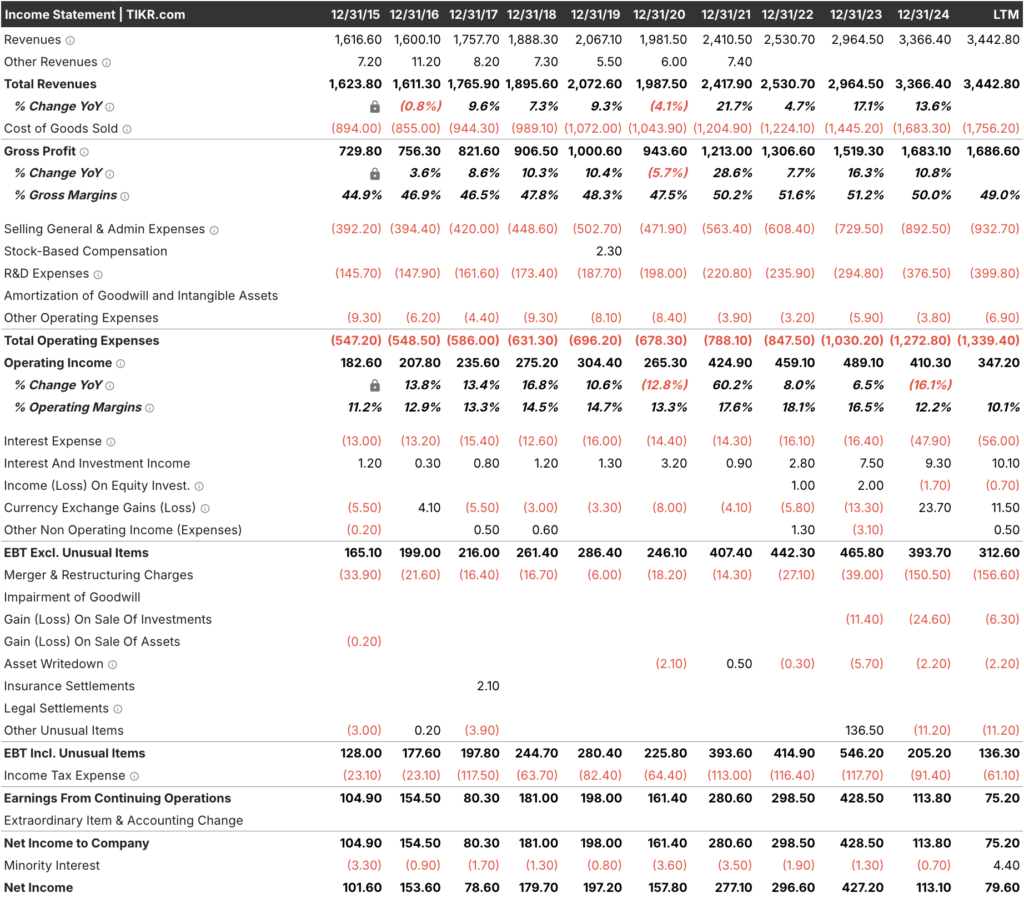

Source: TIKR – Bruker Corp. Income Statement, from 2015 to 2024

Bruker has demonstrated strong results over the last 10 years by keeping high and consistently growing Revenue, but also, sustainable Gross Margins which have been greater than 44% since 2015, which is a really positive indicator of a healthy business.

The increase on “Merger and Restructuring Charges” reduced significantly the Net Income on 2024, the reason behind this decrease is related to

In 2020, while the operating expenses did not raised, the Operating Income decreased by (12.8%) as a result of World Wide Health crisis. On the other hand, the Operating Margins have been double-digit over the last 10 years.

Burker has a positive liquidity ratio, if we take a look at its current assets vs. current liabilities, over the last 10 years the company has been above 1.2, which I consider a good ratio, and it tells us its capacity to generate liquidity in a short-term period. On the other hand, their Inventory and Net Income growing trend demonstrates a healthy and correlated selling cycle, where the volumes are still reasonable.

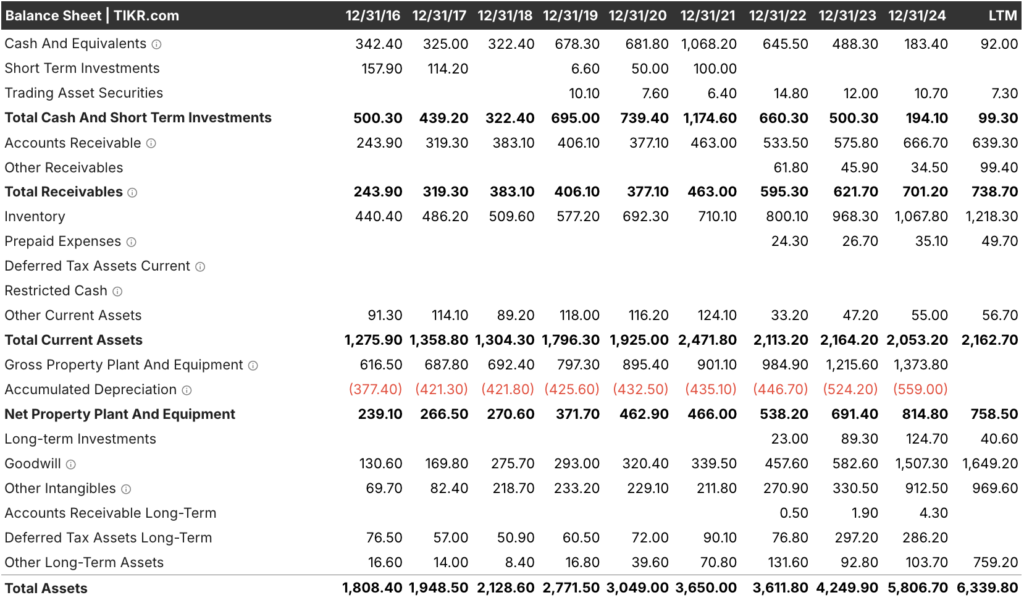

Source: TIKR – Total AssetsSource: TIKR – Total Liabilities and Total Equity

Valuation

Source: TIKR PE Ration Bruker Corporation vs Thermo Fischer.

Burker is currently valuated at 27% EV/EBITDA.

Instrinsic Value

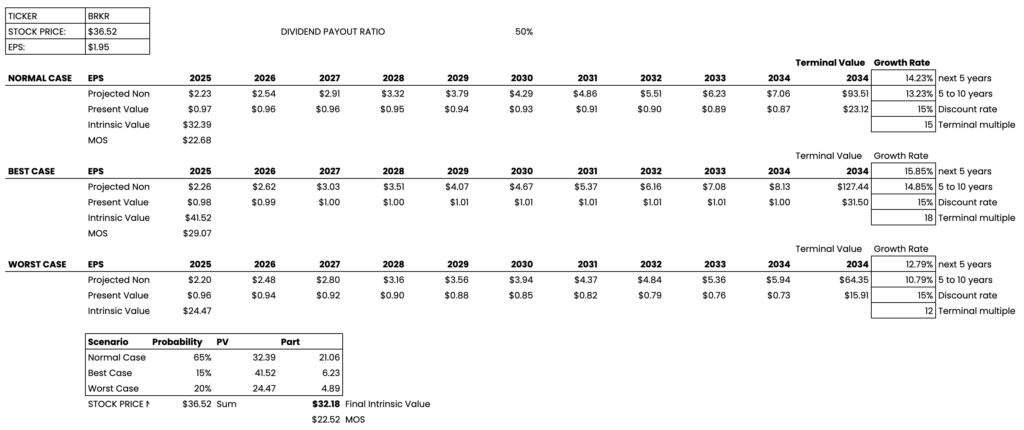

Based on a simplified Discounted Cash Flow (DCF) model, Bruker Corporation (BRKR) appears to be significantly undervalued. With a current stock price of around $30, our analysis, using a 15% discount rate and our three different scenarios, estimates the intrinsic value to be approximately $32.18 per share, approximately.

Discounted Cash Flow (DCF) Model by Earnings Multiples Valuation, own production.

The analysis indicates that BRKR is overvalued at its current price of $37.24, given that the calculated intrinsic value is approximately $27.35. This suggests that the market is valuing the company beyond its ability to generate future earnings. The multiples and ratios (P/E, P/B, ROE) should be compared with industry averages to assess whether they are in line with the company’s maturity. In this case, the margin of safety is insufficient, indicating significant risk for investors.

Based on the analysis performed, I consider BRKR to be overvalued. Despite a history of growth and a healthy ROE, the current share price does not adequately reflect its intrinsic value. Growth projections, while optimistic, present a considerable risk of not being met. Therefore, I would recommend that investors be cautious and consider waiting for a more attractive price before making a purchase.

Overall Summary

BRKR shows solid fundamentals, but the current price does not justify its intrinsic value. The company could be an option to consider in the future if the price adjusts to a more reasonable level.

“Buffettology” proves to be an invaluable resource for beginners venturing into the world of long-term investments. The book strikes a balance between accessibility and depth, offering a clear and concise exploration of key concepts in value investing.

The strength of the book lies in its ability to demystify the complexities of value investing, providing readers with a straightforward and comprehensible guide that will allow them to better identify good companies and make decisions from a “business sense” point of view.

Even for those with limited financial knowledge, the author breaks down Warren Buffett’s investment philosophy into easily digestible components, making it an ideal starting point for individuals looking to build a strong foundation in long-term financial strategies.

The inclusion of real-world investment examples further enhances the book’s value. By dissecting successful investment decisions made by Warren Buffett, “Buffettology” provides readers with practical insights into the thought processes and strategies that have consistently contributed to his wealth-building success.

These examples serve as compelling illustrations of how the principles of value investing can be applied effectively.

However, it’s important to note that the book does have a tendency to be repetitive. While the repetition may help reinforce certain concepts, it could potentially be a drawback for readers who prefer a more streamlined narrative.

Despite this, the overall clarity and the wealth of investment examples make “Buffettology” a worthwhile read for those seeking to understand the nuances of long-term investing, especially from the perspective of one of the most successful investors in history.

I would like to mention that the mathematical tools that this book offers are a good starting point for measuring the returns of our investment from a long-term point of view, that’s why I’ve built this spreadsheet that will allow you to start doing your first calculations and returns on your investment

In conclusion, “Buffettology” stands out as a commendable choice for beginners interested in long-term investments. Its user-friendly approach, coupled with insightful investment examples, offers a solid introduction to the principles of value investing, even though some readers may find the occasional repetition a minor drawback.

“Warren Buffett: The Interpretation of Financial Statements” by Mary Buffett and David Clark is not your typical finance book – it’s a thrilling journey into the world of money and investing with none other than the legendary Warren Buffett as your guide. With this book, you’ll embark on an exhilarating ride through the intricate web of financial statements, armed with the knowledge to make your investments soar.

First off, buckle up for the introduction where you’ll meet the maestro himself, Warren Buffett. Picture a financial superhero who wears a cape made of annual reports and carries a briefcase filled with balance sheets. He’s the ultimate champion of long-term investing, and you’re about to learn his secrets!

The beauty of this book lies in its ability to make complex financial concepts as entertaining as a blockbuster movie. Whether you’re a Wall Street wizard or just starting your investment journey, you’re in for a treat.

Now, let’s dive into the real action: the financial statements. Think of the balance sheet as a treasure map. Mary and David guide you through the maze of assets, liabilities, and equity, helping you uncover hidden treasures of financial stability and growth potential. You’ll learn how to spot financial landmines like excessive debt and how to tell the good assets from the not-so-good.

And did I mention the real-life case studies? These are like thrilling episodes from Warren Buffett’s investment adventures. You’ll witness his triumphs and missteps, gaining valuable insights that you can apply to your own investment escapades.

One of the coolest takeaways from the book is the concept of “economic moats.” It’s not a medieval defense structure, but it’s equally powerful. Think of it as a force field that protects a company’s profitability. Understanding economic moats is like finding the secret sauce that makes some businesses unstoppable.

If there’s one thing this book emphasizes, it’s patience. Warren Buffett is the ultimate patient investor, and you’ll learn why that’s so important. It’s like learning to savor a fine wine instead of chugging a soda – a change in perspective that can revolutionize your investing game.

In a world filled with complicated finance textbooks, “Warren Buffett: The Interpretation of Financial Statements” is like a breath of fresh air. It keeps things light, fun, and exciting while delivering invaluable financial wisdom.

In conclusion, “Warren Buffett: The Interpretation of Financial Statements” is like a rollercoaster ride through the financial universe with Warren Buffett as your trusty tour guide. Whether you’re a financial novice or a seasoned investor, this book is like a golden ticket to understanding the magic behind financial statements. With Warren Buffett by your side, investing becomes an adventure, and financial analysis transforms into a thrilling quest for hidden treasures. So, grab your hat, hop on the Buffett express, and get ready for a financial adventure of a lifetime!

Fortinet was founded in 2000 and is headquartered in Sunnyvale, California. The company provides broad, integrated, and automated cybersecurity solutions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Introduction

Fortinet provides security subscriptions, technical support, and professional, and training services. It sells its security solutions to channel partners and directly to various customers in telecommunications, technology, government, financial services, education, retail, manufacturing, and healthcare industries.

FortiGate hardware and software licenses that provide various security and networking functions, including firewall, intrusion prevention, anti-malware, virtual private network, application control, web filtering, anti-spam, and wide area network acceleration.

FortiSwitch product family, offers secure switching solutions for connecting customers to their end devices.

The FortiAP product family, provides secure wireless networking solutions.

FortiExtender, a hardware appliance.

FortiAnalyzer product family, which offers centralized network logging, analyzing, and reporting solutions.

FortiManager provides a central and scalable management solution for its FortiGate products.

FortiWeb provides web application firewall solutions.

FortiMail secures email gateway solutions.

FortiSandbox technology delivers proactive detection and mitigation services.

FortiClient provides endpoint protection with pattern-based anti-malware, behavior-based exploit protection, web filtering, and an application firewall.

FortiToken and FortiAuthenticator product families for multifactor authentication to safeguard systems, assets, and data.

FortiEDR/XDR, is an endpoint protection solution that provides both comprehensive machine-learning anti-malware execution and real-time post-infection protection.

Revenue by Geography (Q2 2023)

According to their last earnings call, we see how Fortinet has been gradually increasing revenue in all territories since 2021, and Americas is the highest revenue provider compared to EMEA and APAC.

Source: Fortinet Inc. – Q2 2023 Financial Results, Revenue by Geography

Market Research and Forecast

Source: Technavio – Global Cybersecurity Market 2021-2025

The global Cybersecurity market has been growing since 2018, especially in North America, Europe, and Asia Pacific, where the North American market is the sector’s most important demand and where Fortinet has more get the vast majority of its revenue. According to Polaris, North America will still be the leading region until 2030, followed by Europe and Asia Pacific.

Security Services dominates the market with a projected market volume of US$87.97bn in 2023.

Source: Statista – Revenue by Component, Sep 2023

The three main cybersecurity consumer groups are the banking and IT and telecom industries followed by Governments, where logically this last group leads the demand, according to GM Insights.

Source: GM insights

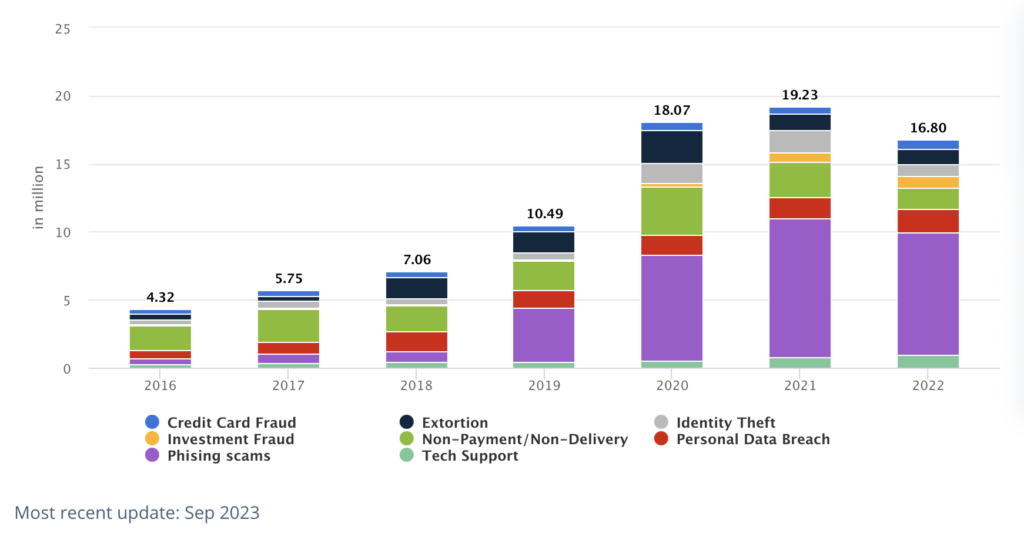

Another factor to take into consideration that explains the demand for cybersecurity services is the continuously growing trend of cyberattacks, where phishing scams took the lead in 2019.

Source: Statista – Recorded Cyberattacks, Sep 2023

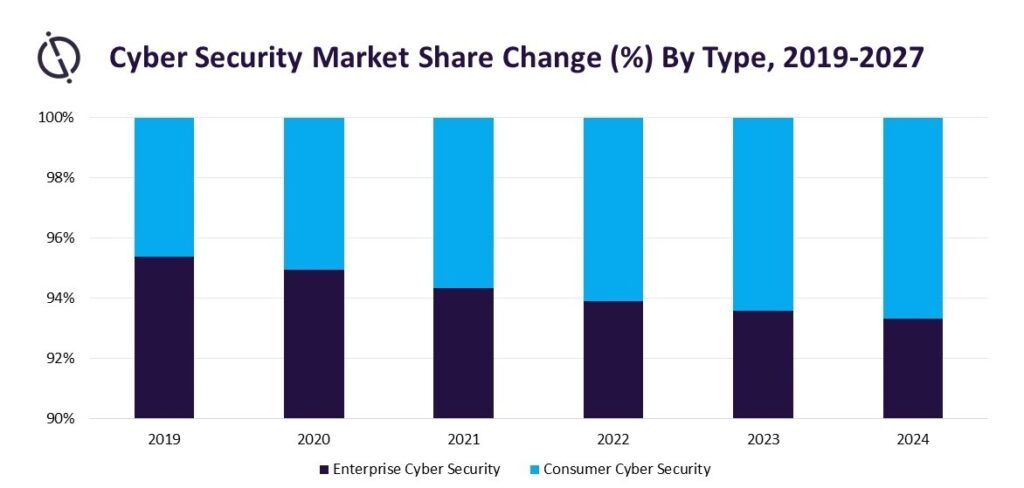

That being said, and according to Globaldata, we can see a change in the current paradigm where Consumer Cybersecurity is expected to grow and take more market share than the Enterprise demand.

Source: GlobalData Technology Intelligence Center

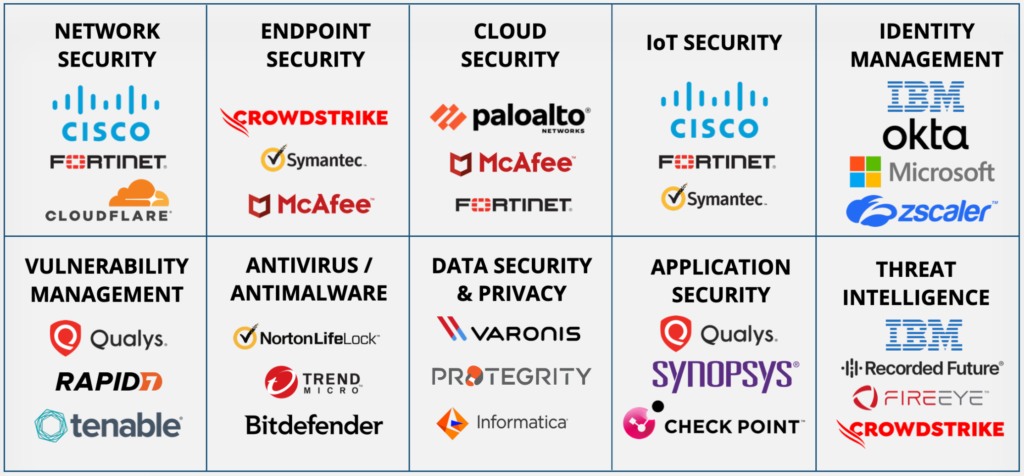

Finally, in the image below you will find how the cybersecurity market is composed (and how big it is). According to Fortinet, the main company business pillars are Network Security, Cybersecurity, Cloud Security, and OT Security.

Source: App Economy Insights, Jun 2023, CyberSecurity Market Map

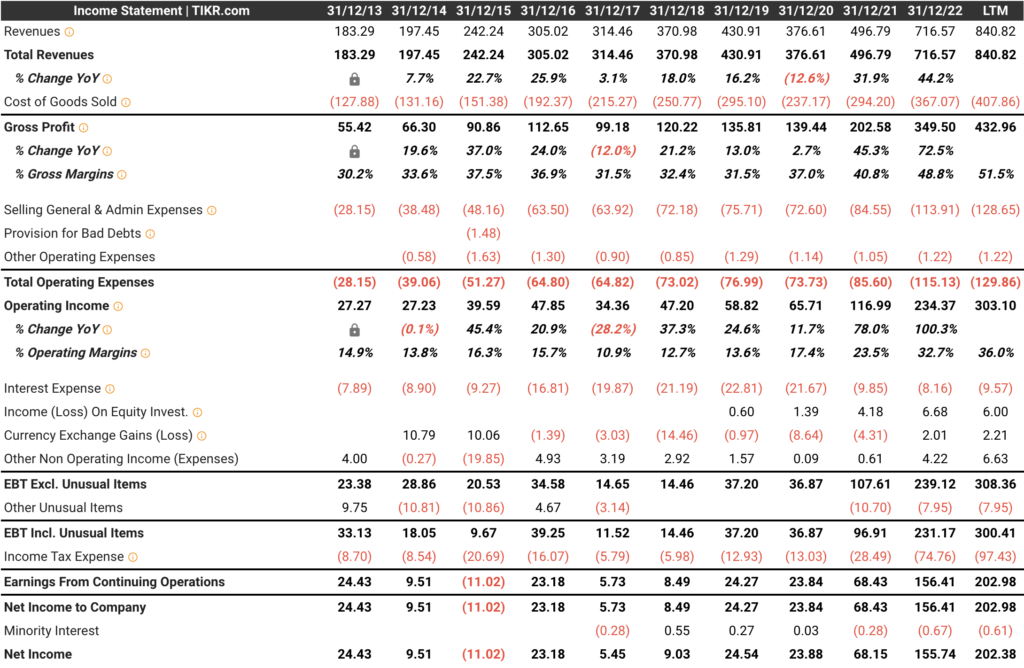

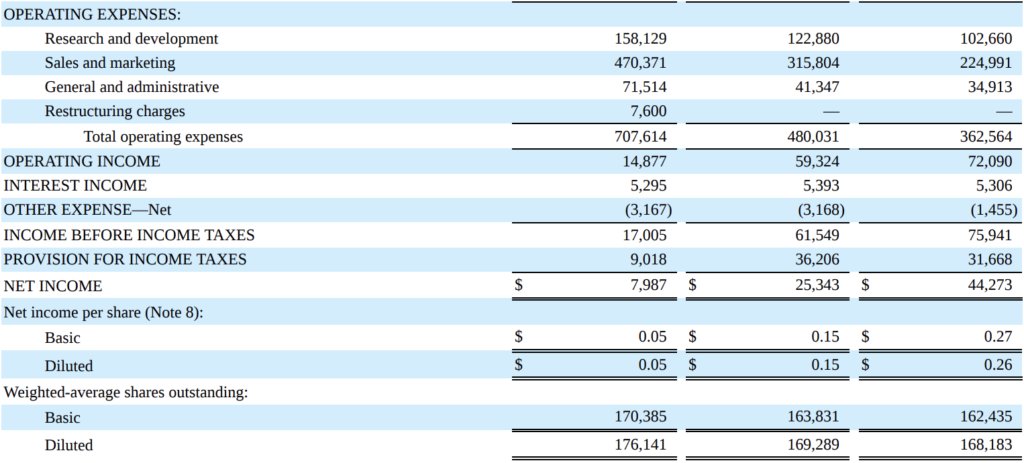

Fortinet Income Statement

Source: TIKR – Fortinet Income Statement, from 2013 to 2022

Fortinet has demonstrated strong results over the last 10 years by keeping high and consistently growing Revenue double-figure and greater than 29% since Q2’21 according to their last Q223 Earnings Call, but also, sustainable Gross Margins which have been greater than 70% since 2013, which is a really positive indicator of a healthy business.

In 2014 and 2015, with the operating expenses raised, the Operating Income decreased by (21.9%) and (57.1%).

The Sales and Marketing and General and Administrative were the items that received the greatest investment, taking into account its Annual report (10K):

“In 2015, we continued to invest in sales and marketing to capture market share, particularly in the enterprise market where enterprise customers tend to have a higher lifetime value, and to accelerate our growth. We intend to continue investing in sales and marketing in order to capture additional market share in the enterprise market”.

The global sales and marketing employee footprint increased from 41% in Q1 to 44% in Q4, as well as their investment, according to the company’s quarterly reports:

“In 2015, operating expenses increased by $227.6 million, or 47%, as compared to 2014. The increase was primarily driven by our accelerated pace of hiring and continued investments to expand our sales coverage, grow our marketing capabilities, develop new products and scale our customer support. We also continue to invest in research and development to strengthen our technology leadership position. We believe that continued product innovation has strengthened our technology and resulted in market share gains. In addition, we incurred costs from the integration of Meru and the implementation of restructuring activities and expenses related to business design and reengineering in preparation of an ERP system implementation. Headcount increased by 41% to 4,018 employees and contractors as of December 31, 2015, up from 2,854 as of December 31, 2014.“

Source: Fortinet 10-Q

Source: Fortinet Inc. – Form 10K 2016 – CONSOLIDATED STATEMENTS OF OPERATIONS

In regard to the headcount increase, in July 2015, Eric Mann and Mike Bossert joined the company’s leadership team, as sales vice presidents focused on continued expansion and growth of the enterprise and mid-enterprise market segments, and in September of the same year, Fortinet announced that Holly Rollo joined as Chief Marketing Officer.

Additionally, the company expanded its patent portfolio to more than 200 patents.

Back in 2018, we can see positive Income Tax Expenses as a result of effective tax rate benefits.

Our provision for income taxes for 2018 reflects an effective tax rate benefit of (32)%, compared to an effective tax rate provision of 75% for 2017. The benefit from income taxes for 2018 was comprised primarily of impacts related to the 2017 Tax Act including a benefit of $164.0 million from the realignment of our tax structure and operations that resulted in a book-to-tax basis difference from previously taxed off-shore deferred revenue. These benefits were partially offset by a $32.6 million increase in the transition tax for finalization of the provisional estimates under SAB 118, a $20.5 million tax expense for the impact of the GILTI and a $29.6 million of tax expense related to U.S. federal and state taxes, other foreign income taxes, foreign withholding taxes and a decrease in tax reserves. Effective January 1, 2018, the 2017 Tax Act reduced the federal corporate income tax rate from 35% to 21% and created a territorial tax system with a one-time mandatory tax on foreign earnings of U.S. subsidiaries not previously subject to U.S. income tax. Under GAAP, changes in tax rates and tax law are accounted for in the period of enactment and deferred tax assets and liabilities are measured at the enacted tax rate. In December 2017, the SEC staff issued SAB 118, which allowed us to record provisional amounts during a measurement period not to extend beyond one year of the enactment date. As a result, we previously provided a provisional estimate of the effect of the 2017 Tax Act in our financial statements. In the fourth quarter of 2018, we completed our analysis to determine the effect of the 2017 Tax Act within the measurement period under the SEC guidance, and reflected an increase of an additional $32.6 million related to the transition tax in the 2018 income tax expense. We expect further guidance may be forthcoming from the FASB and the SEC, as well as regulations, interpretations and rulings from federal and state tax agencies, which could result in additional impacts. In 2017, the effective tax rate was 75%, primarily resulting from the deferred tax assets remeasurement and a one-time transition tax due to the 2017 Tax Act. Excluding the tax impacts from the 2017 Tax Act, our 2017 effective tax rate would have been 24%.

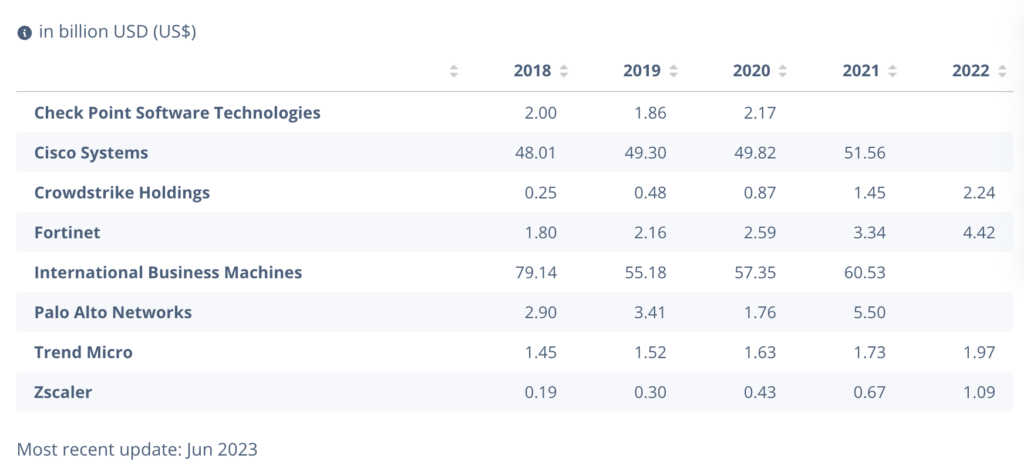

According to a report from Statista released in June 2023, Fortinet has built on an upward revenue trend from 2018 to 2022 that has allowed it to expand and distance itself from some of its competitors, that being said, the company is still far from big players like Cisco or International Business Machines but its constant and bullish trend is a good sign of thriving business, especially if we take into account the external factors on 2020 and how negatively impacted in some business, due to Fortinet biggest factories are in Taiwan and China.

Source: Statista – Top company revenues (Worldwide & Consolidates) – Jun 2023

On the other hand, According to IDC (the world’s leading provider of market intelligence, consulting services, and events for the Information Technology, Telecommunications, and Consumer Technology markets), Fortinet Firewall division solution surprises in Revenue market share in 2022 to Palo Alto Network, Cisco and Check Point and kept a comfortable distance in 1QC 2023.

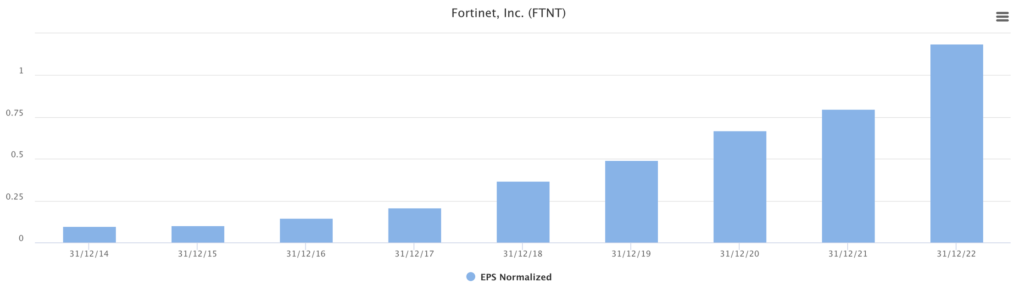

Fortinet has reported sustainable EPS growth (37% average CAGR from 2015 to 2022).

Source: TIKR – EPS Normalized

If we take a look at their Operating Expenses in 2023, we should take into account that Fortinet has a total of 1,285 global patents (as of June 30, 2023) and 254 Pending Patents, which makes me better understand the continuous increase is logical together with the development of new technologies, may affect the raise. I do not consider a concerning figure for the sales and marketing item taking into account the YoY growth from the last 6 years of Revenue and the Gross Margins as we mentioned earlier.

Source: Fortinet Inc. – Form 10K 2022 – Consolidated Statements of Operations

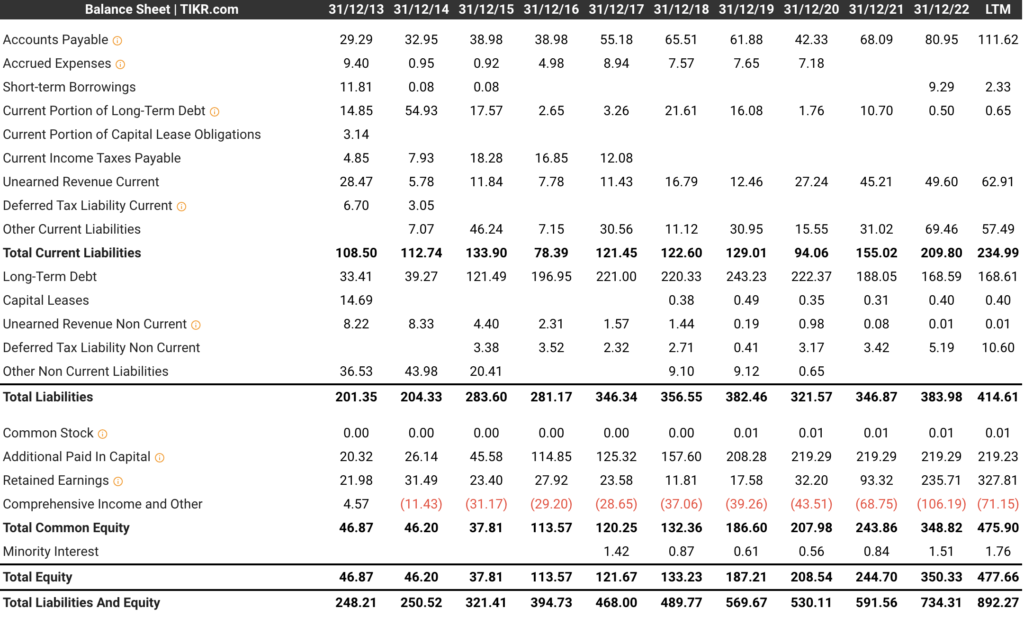

Balance Sheet

Fortinet has a positive liquidity ratio, if we take a look at its current assets vs. current liabilities, over the last 10 years the company has been above 1.2, which I consider a good ratio, and it tells us its capacity to generate liquidity in a short-term period. On the other hand, their Inventory and Net Income growing trend demonstrates a healthy and correlated selling cycle, where the volumes are still reasonable.

Source: TIKR – Fortinet Assets Statement, from 2013 to 2022Source: TIKR – Fortinet Total Liabilities and Equity Statement, from 2013 to 2022

Long-term debt increase in 2021 comes from a Senior Notes offering where the company priced a $1 billion debt offering ($500 million in 1.000% notes due 2026 and $500 million in 2.200% notes due 2031). Additionally, the company reduced the amount of shares starting in March.

In July 2020, our board of directors approved a $500.0 million increase in the authorized stock repurchaseamount under the Repurchase Program and extended the term of the Repurchase Program to February 28, 2022, bringing the aggregate amount authorized to be repurchased to $3.0 billion.

Source: Fortinet Inc 10-Q

Our principal commitments consist of obligations under our Notes, inventory purchase and other contractual commitments. As of December 31,2021, the long-term debt, net of unamortized discount and debt issuance costs, was $988.4 million. In addition, we enter into non-cancellable agreements with contract manufacturers to procure inventory based on our requirements in order to reduce manufacturing lead times, plan for adequate component supply or incentivize suppliers to deliver. In 2021, we significantly increased these commitments as contract manufacturers and component suppliers significantly increased their pricing and lead times. Inventory purchase commitments as of December 31, 2021, were $1.14 billion, an increase of $881.1 million compared to $259.4 million as of December 31, 2020. We estimate payments of $1.08 billion due on or before December 31, 2022 related to these commitments. We also have open purchase orders and contractual obligations in the ordinary course of business for which we have not received goods or services. As of December 31, 2021, we had $126.7 million in other contractual commitments having a remaining term in excess of one year that are non-cancelable.

Source: 10-K Fortinet Inc 2021

As we mentioned earlier, the pandemic hit multiple businesses (and created other investment opportunities). In 2021, and because of the pandemic, this impact on the manufacture of semiconductors in South Korea and Taiwan was cited as a cause for the shortage, so my understanding is that in order to guarantee the supply, the company.

Reviewing the investments line item, I found two big ones around 2021.

The first one is Linksys Holdings, Inc. (“Linksys”), where Fortinet invested $160 million in cash for shares of the Series A Preferred Stock of privately held representing a 50.8% ownership interest in the outstanding common stock (on an as-converted basis). Linksys provides router connectivity solutions to the consumer and small business markets, that being said, its sales have declined since Fortinet started its investment.

Last but not least, between 2021 and 2022 Fortinet executed a strategic acquisition of Alaxala Networks Corporation, a privately held network hardware equipment company in Japan, for $77.7 million in cash. According to Fortinet:

We acquired the equity interests in Alaxala to broaden our offering of secure switches integrated with our Core Platform and Enhanced Platform Technology functionality and over time, to innovate and rebrand certain of Alaxala’s switches to offer a broader suite of secure switches globally.

The company has good short-term liquidity ratios, especially the Current Ratio (total current assets / total current liabilities) which has been above 1 since 2013 and explains its power to pay down the current liabilities.

Source: TIKR – Fortinet Short Term Liquidity, from 2013 to 2022 (respectively)

Competitors’ Pros and Cons

Fortinet’s competition is spread around the world, some names are Arista Networks, Inc., Aruba Networks, LLC, Barracuda Networks, Inc., Check Point Software Technologies Ltd., Cisco Systems, Inc. (“Cisco”), CrowdStrike Holdings, Inc., F5 Networks, Inc., Huawei Technologies Co., Ltd., Juniper Networks, Inc., Palo Alto Networks, Inc., SonicWALL, Inc., Sophos Group Plc, Trend Micro Incorporated, VMware, Inc. and Zscaler, Inc. (“Zscaler”). I believe that Fortinet has a competitive advantage over its competitors, these are some examples that led me to think so:

Some companies have been reporting negative Net income over the last seven and then years

Big corporations are growing slowly, which is understandable due to their global presence

Long-term debt. I try to find companies with low long-term debt levels, but some of them have not been able to decrease it (Fortinet is not exempted). That being said, the big players with enough earning power have the advantage of being able to meet their long-term debt payments

Liquidity levels are a bit concerning across some of their competitors, they will struggle to convert assets to pay their liabilities

But, these companies can perform better in some KPIs and have advantages:

Better margins, above 80%

The gap between Price and EPS is bigger than Fortinet, so they can potentially be undervalued if we compare it to their capacity to generate value for the investor

Bigger budgets to invest in sales, marketing, and IT

Important, Brand recognition. I do not need to mention which ones are more well-known than others

Switching costs are key in this industry, especially if we take into account the enterprise customer and the investment in training

Fortinet’s Ownership

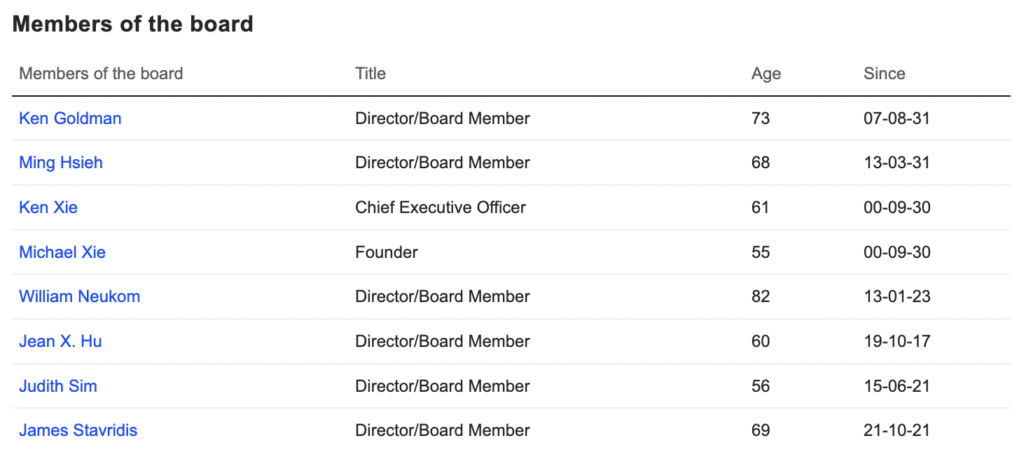

Fortinet’s CEO Ken Xie, the founder of the company, holds more than 63M shares (8% of shares outstanding held), and her brother Michael Xie, who also holds 69M (8.85% of shares outstanding held) which is a good sign not only because both have key roles in the company but also because the Xie family keeps a big share of the company, and convey a solid alignment between their and the company’s interests.

Source: Market Screener – Members of the board

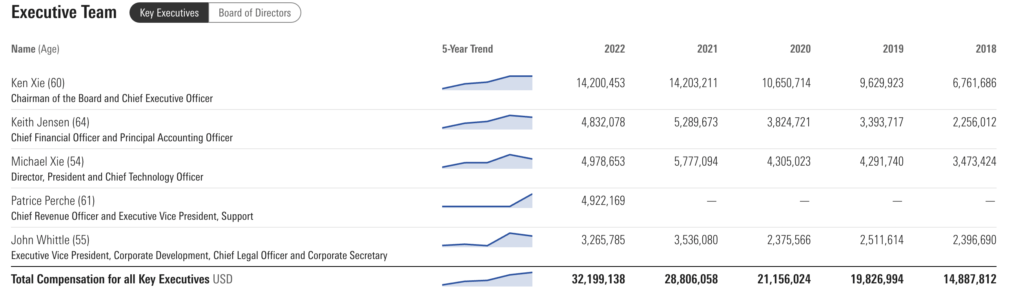

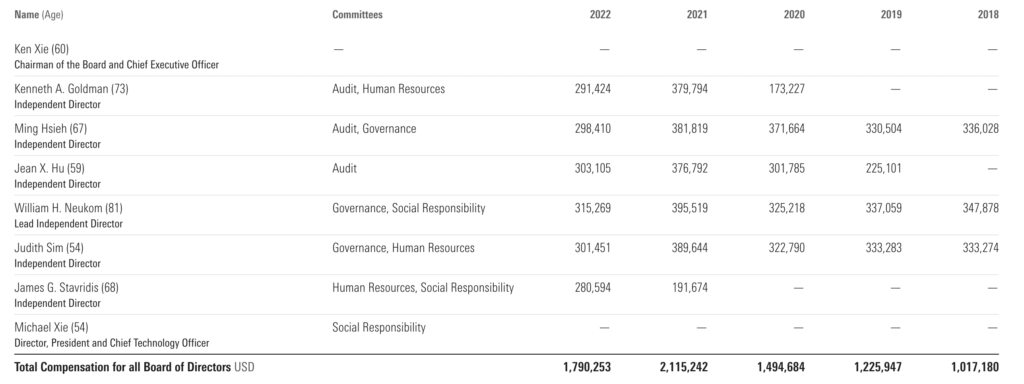

Below, I’ve included a snapshot of Fortinet’s Key Executives and Members of the Board Director, along with their yearly compensation. None of the stakeholders makes more than 10% in revenue, which is a positive sign and it makes me feel that the leadership team is not squeezing the organization funds.

Source: Morningstar – Total Compensation for all Key ExecutivesSource: Morningstar – Total Compensation for all Board of Directors

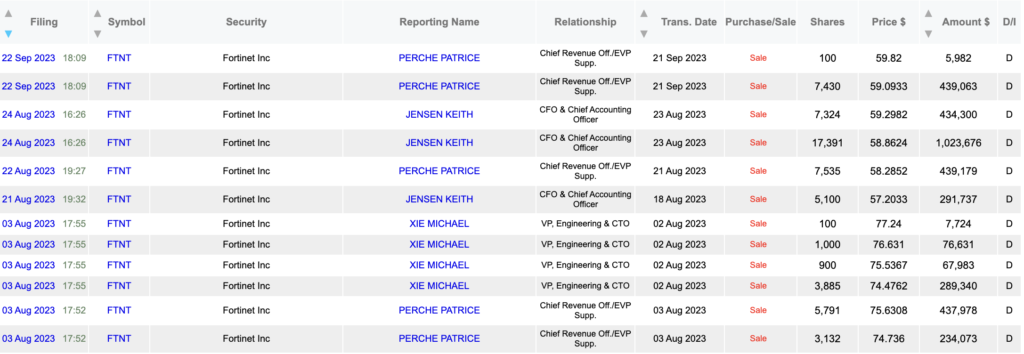

Regarding the Insiders, we have not identified unexpected movements or aggressive sales from the Executive team or board of Directors.

Source: Data Roma, Insiders Sells, last 3 months 2023

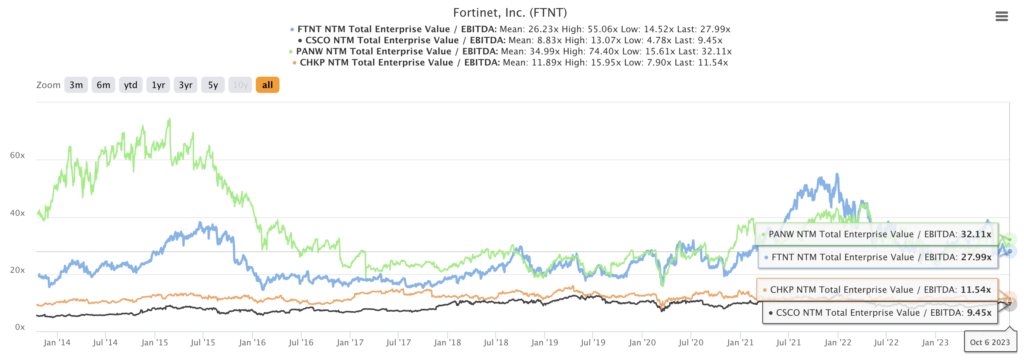

Valuation

Fortinet is currently valuated at 27% EV/EBITDA. Although I believe the company does not have an attractive valuation, I would mention some key things.

First of all, the revenue is projected to grow at double-digit and above >20%, the company is doing a great job so I consider it not exaggerated.

The valuation is not at all-time highs, even though this is not a metric that by itself doesn’t tell me anything, the drop in we have observed it’s due to how fragmented is the market and how unclear is for Mr.Market to buy Fortinet or other cybersecurity companies.

Reviewing its main competitors, we should break down them by like Check Point Software and Cisco, big corporations growing <10% every year with expanded worldwide, and Fortinet and Palo Alto Networks, where personally I do think Fortinet has better and robust financial health.

Source: TIKR – NTM Total Enterprise Value / EBITDA

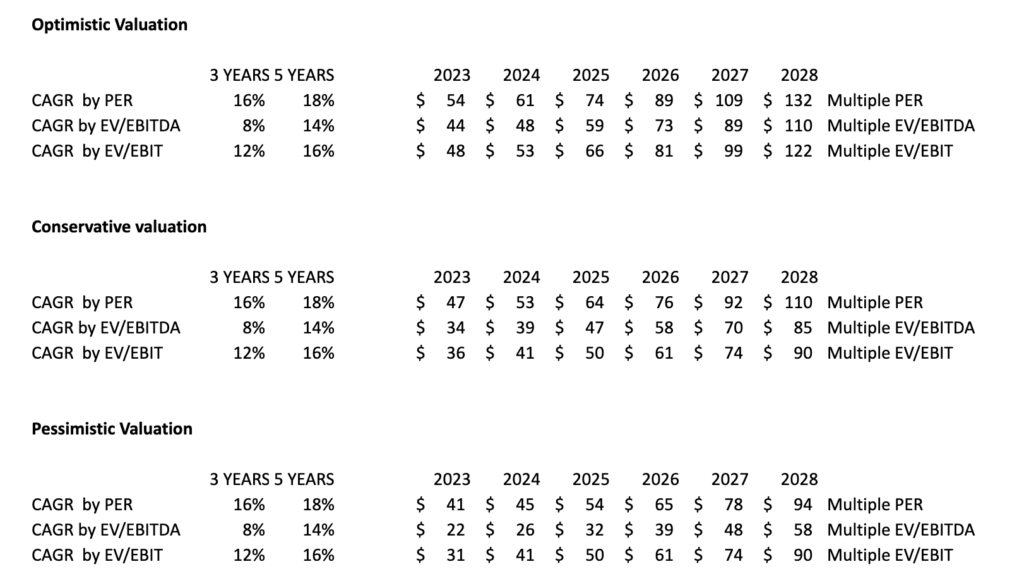

So, let’s talk about the (my) valuation.

I’ve built three scenarios by taking into account different PER, EV/EBITDA, and EV/EBIT valuations. I took into account the lowest, mid, and highest valuations not only from Fortinet but also from its competitors. To be honest, I will take into account the EV/EBITDA instead of the PER.

Final Comments

The software industry is usually considered a monopoly business model where “Winner Takes All”, and where the cybersecurity market is very fragmented.

Big competition means that at some point, there exists the possibility that some companies with a worse competitive advantage will increase debt as they cannot self-finance if they need funds for investments like acquiring new companies, adding more resources to increase sales, or IT to develop new technologies or finance patents.

Fortinet’s revenue forecast CAGR (5y) is 18.8%, which is above the 15% I consider the minimum CAGR the market average and my security margin.

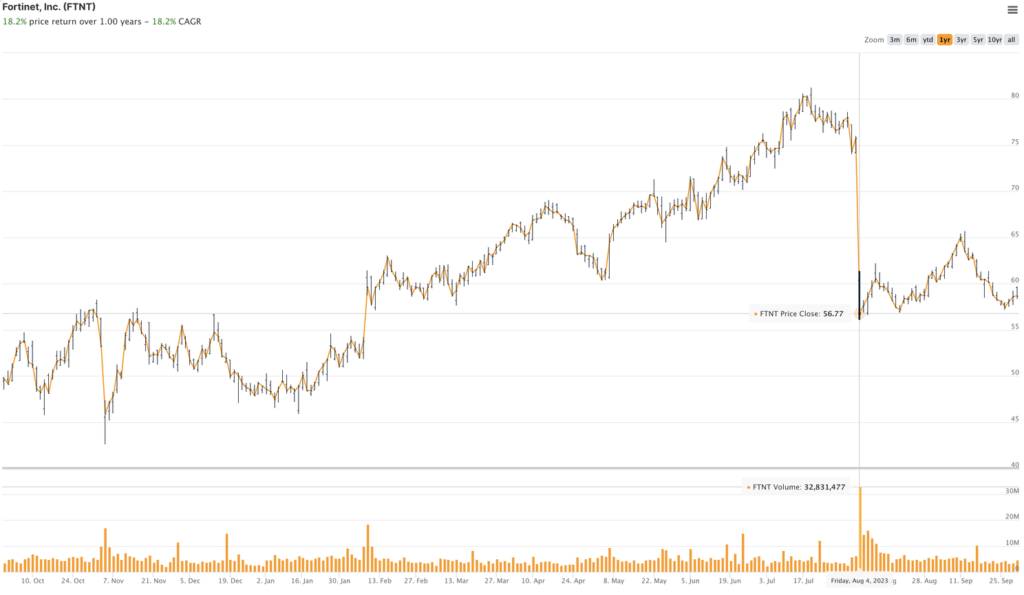

On August 3rd, the company announced earnings and the share price decreased from $75.76 to $56.77/share (-28.65%), after the company confirmed to expect total revenue in the range of 5.35 billion to 5.45 billion for the fiscal year 2023, a lower figure from a prior view of $5.43 billion to $5.49 billion.

Source: TIKR, Fortinet Inc. (FTNT)Source: DataRoma, Fortinet Sells, Q2 2023

But when we take a look at the share price evolution but also the NTM Normalized Earnings per share, there is a healthy correlation between the price and the earnings growth, showcasing Fortinet’s value generator and its capacity to recover its share price in 2020 despite the global pandemic, so the drop in the stock price could be influenced by the fact that there is not a clear leader in the industry, and that can easily affect the investor’s perception vs the companies strength to capture the pole position.

Source: TIKR, Price vs. NTM Normalized Earnings per Share

That being said, the initial rate of return is not attractive (1.57$/58=2.7%), so to see an interesting rate of return figure around 12%, the price should have a correction of around 50%, and the earnings per share should increase up to 3.5$.

These books helped me to better understand the value investing: